Don't fight the SPR

A wall of oil is being released

In this report: Why Brent fell 12% this week, when the OECD release tapers off, and the political escalation the market is missing. The calendar trade for what comes after.

Last week Brent: -11.86% (-$12.36). Open $97.50 High $97.81 Low $89.93 Close $91.89

Articles

Video: Jeff Currie on potential U.S.-Iran peace deal: Sell the tweet, buy the molecule

LNG Tanker Exits Hormuz For India For First Time Since War Began to EU ports

Why the real oil shock may only begin when China returns

Canada Strikes Landmark Deal to Export Liquefied Natural Gas to Germany

Oman Leverages its Influence With Iran to Resolve Strait of Hormuz Impasse

Iran Is Tightening Its Grip on the Strait of Hormuz

SPAN Announces XFRA, a Distributed Data Centre Solution

Podcast: Jeremy Grantham on why this market will fall by 50% but nobody will warn you

Podcast: A Perfect Storm Of Troubles Is Brewing | Cem Karsan

Before we get into the report, I am launching the discord server for The Oil Report this week. An email will be sent to paid users for access on Thursday. It will be in soft launch/beta mode through June.

Features are a

Breaking news and curated headline channel.

Forum that has the most up-to-date full EIA analysis with charts.

Forum for COT charts and analysis.

A chat channel -#The Wellhead

Live stage where I will go live at ad hoc points through the weeks

I’ll be in the discord through the week chatting with people once live. I plan to have a live 30-min call with all this Friday on Substack 4pm London time. Hopefully, this will turn into a regular live session if anyone shows up!

View

We have had a nice rhythm to the market since this war began. The US would talk the market into a softening outlook, then Iran would respond, reversing the entire market read to hard stance negotiations. During this time, the market would sell the rumour of a deal being done, then buy the fact that there is no chance of a deal. This price range was approximately- Brent $93 to $110 average $98.50s. WTI $86 to $105 average $94’s. Last week Brent was down 12.6%.

This week, there has been a large shift in this pattern. And here is why.

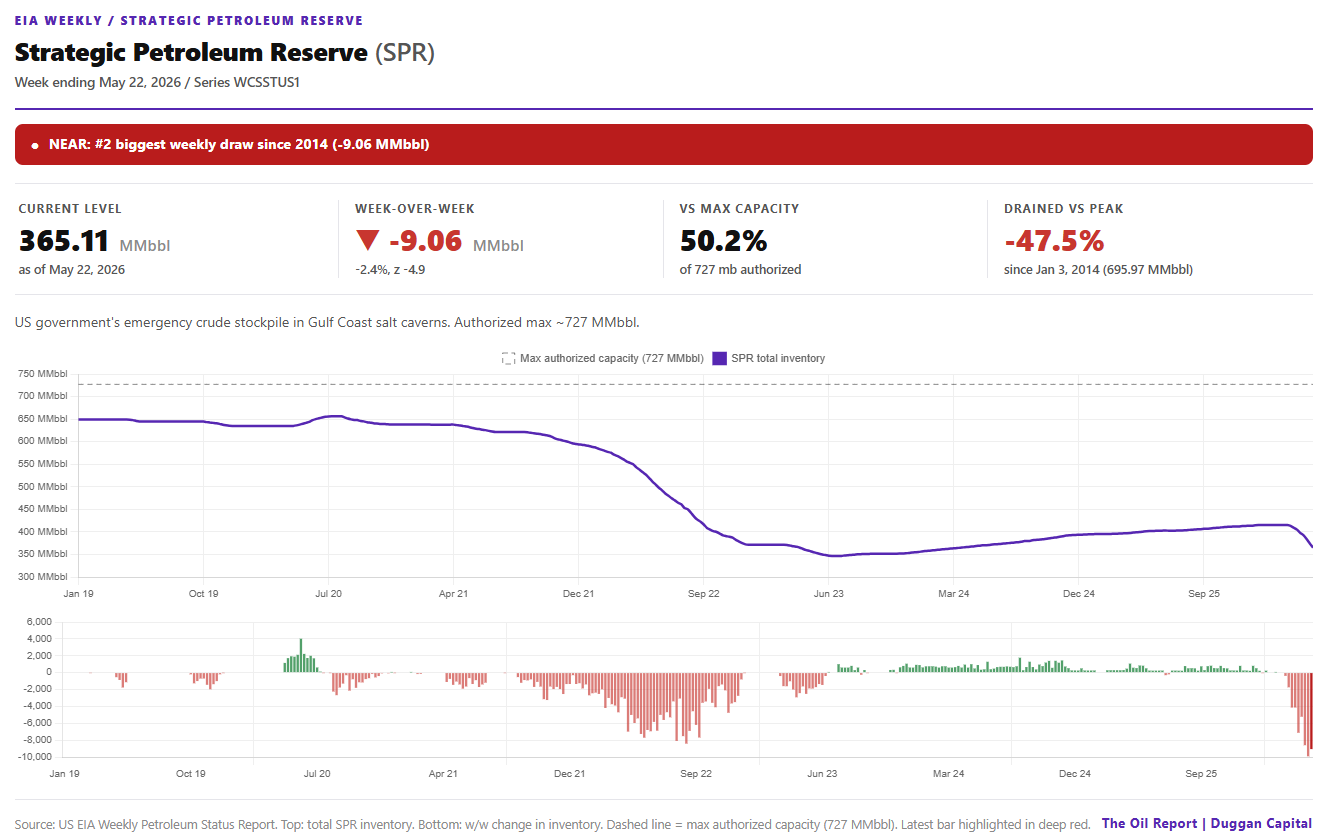

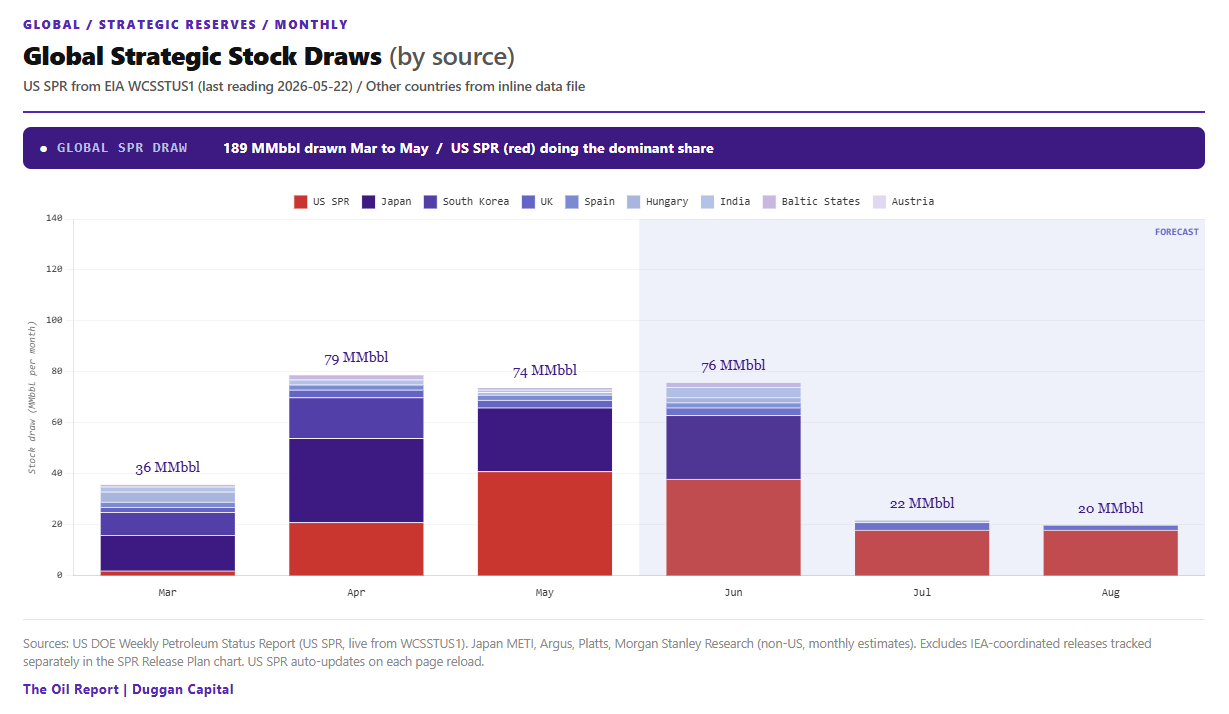

In short, 400mb of oil is feeding into the global system, while the comedy act of deal, no deal plays out in the headlines. The US releasing at a clip of 9mb a week now, translating to a rate of 1.3mb per day! Their share of the 400mb is a total release of 172mb.

In the same way you ‘can’t fight The Fed’, you can’t fight the SPR. It is often at times of extreme volatility, that emergency levers are pulled. During those exceptional times, like in COVID-19, while main street talks intensely about the world ending, Wall Street fades the emergency. In the Dot.com and COVID-19 cases, that was QE (quantitative easing- tons of bailout cash). In this case, it is the SPR release that we trade now, not the fear porn and ‘doom window’ story.

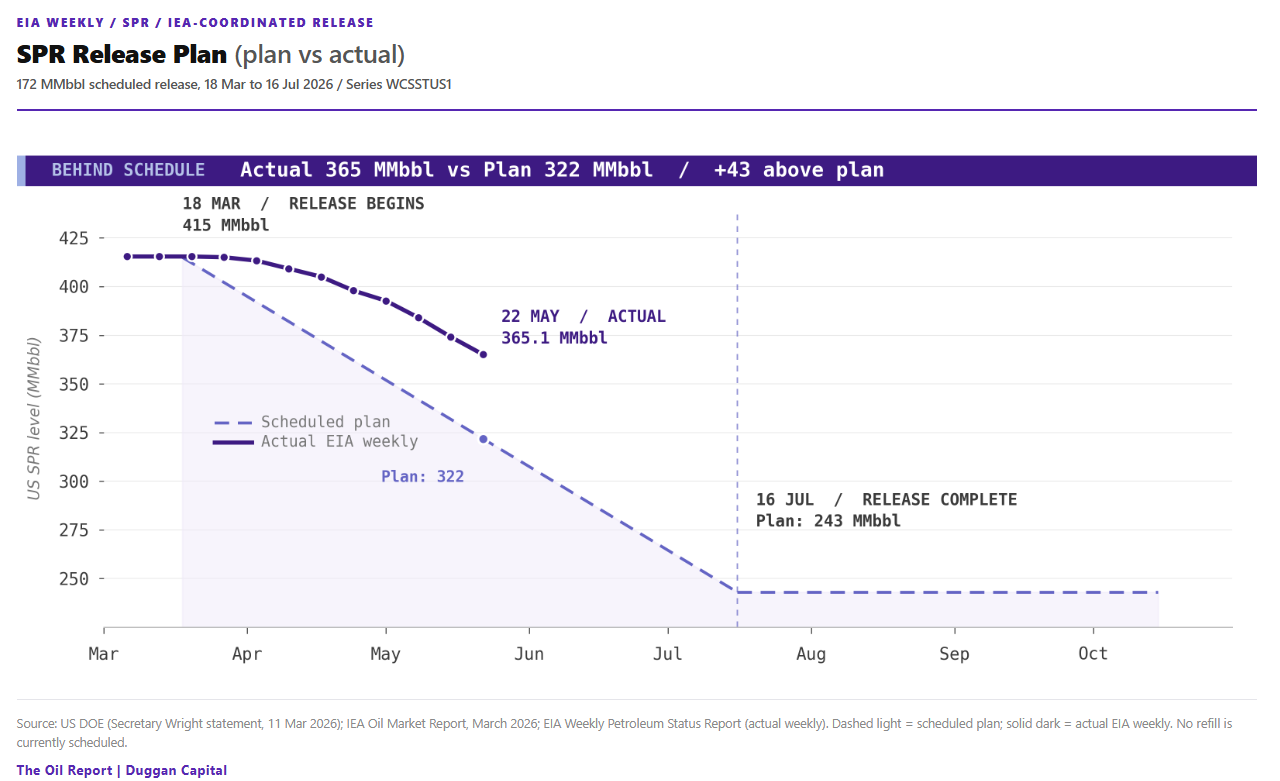

The coordinated OECD release of 400mb has acted to cap prices throughout this entire war so far and still is. The chart below highlights when the US portion (172mb) will be completed.

What I am getting at in this report is simple. I think that until we get to the end of the SPR planned releases, prices are going to shake the ground that we think we are walking on. There are risks to buying the next move. More in trade section below.

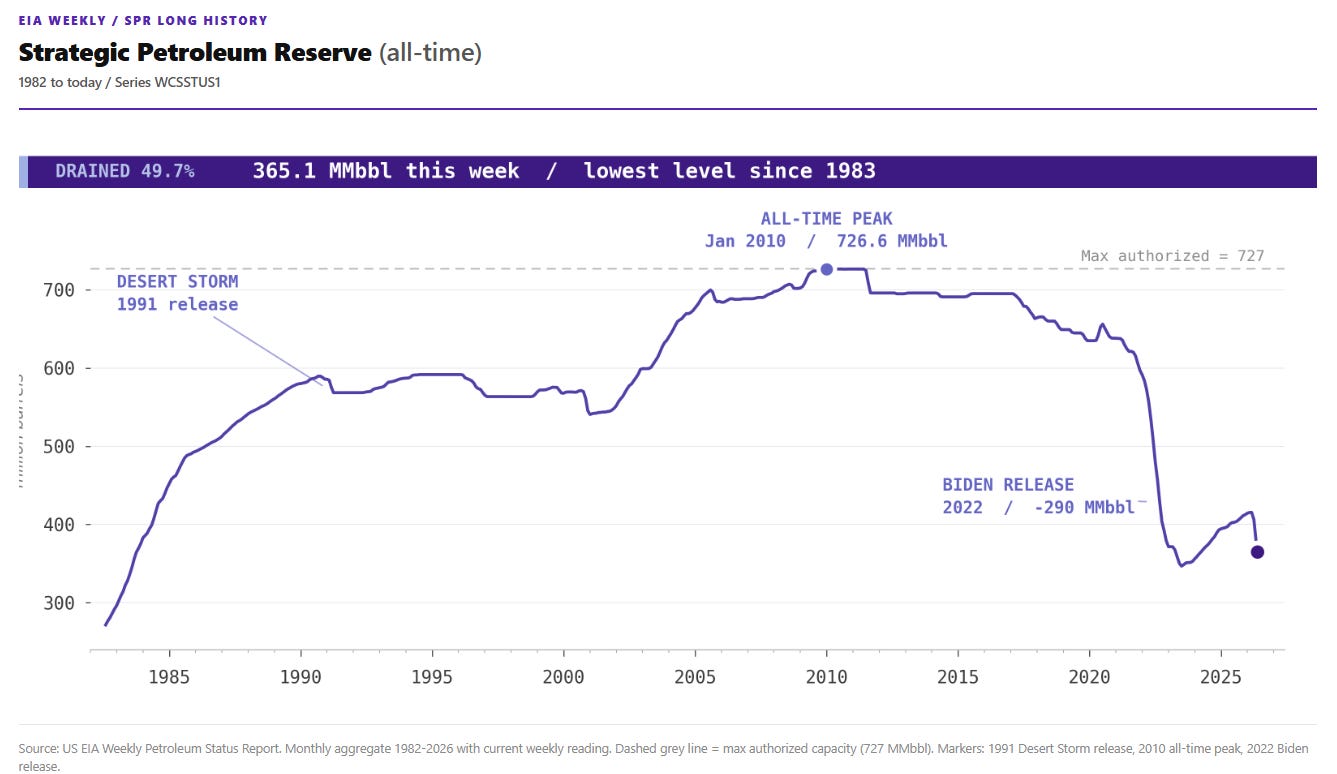

The SPR, while drawing at large levels, will and can survive this. It is still at 50% max capacity.

At the same time, the other acting OECD countries are also releasing. Across all coordinated OECD draws, monthly contributions collapse from 76mb in June to roughly 20mb by August, a three-quarter reduction in the supply that has held this market in range. The releases don’t stop on a single day. It tapers across the summer.

Politics going backwards

It’s been a hell of a week for negotiations. Starting out Sunday with Trump stating that a deal was about to be done, no- seriously this time. Then an AXIOS dreamscape MOU fiasco mid-week, followed by false comments that US ships were to commence escorting ships through the SOH. Net Net, we are MAYBE going to enter a 60-day window of negotiations. With this, it is touted that traffic will resume while the US and Iran hash it out. Iranian red lines remain firm. Nuclear enrichment, the toll booth, a ceasefire between Israel and Lebanon and the sanctions/release of Iranian funds currently tied up. I don’t see any progress being made here. And I don’t see Iran too enthusiastic about resuming traffic to pre-war levels, ie. giving yards when they don’t have to. It is not over.

The US is now placing sanctions on the shiny new PGSA (Persian Gulf Strait Authority). This will work to hamper the Iranian toll booth, in theory. Sanctioning it creates secondary-sanctions exposure for any tanker owner, P&I club, or bank that transacts with it. The flaw is that PGSA was designed to operate completely outside the USD system. Iran’s immediate response was to reframe the toll as an “environmental tax” delivered via a draft Iran-Oman joint protocol, a non-sanctioned cutout via Muscat. Washington responded by threatening Oman directly. Iranian FM Baqaei called that blackmail of a UN member state. Tehran then published the PGSA map, asserting jurisdiction over a maritime zone that extends deep into the UAE and Omani territorial waters, a planted flag, not a negotiating opening. So until The Whitehouse extends those sanctions to include the myriad of workarounds that can occur, the sanctions will be as useful as the prior sanctions were. Not very.

Let’s look at it from an Iranian perspective. Game theory would dictate that they will only actually talk seriously when the US feel the pain. That will be July forward. With this theory, we are in for another 4 weeks of the same from both sides. Deal or no deal.