Equity drag

When Employment Shrinks and Geopolitics Expands

In this report: Oil Slips as Jobs Revisions Shake Confidence; Iranian Risk Remains

Key Stats. WTI -1.09% (-$0.69) for the week. Open $62.99 High $65.83 Low $62.14 Close $62.81

In a pursuit of a world without borders, we opened our doors to an unprecedented wave of mass migration that threatens the cohesion of our societies, the continuity of our culture and the future of our people….This is not an expression of xenophobia. It is not hate. It is a fundamental act of national sovereignty, and the failure to do so is not just an abdication of one of our most basic duties owed to our people. It is an urgent threat to the fabric of our societies and the survival of our civilization itself.’’

Mark Rubio speaking at this weekend’s Munich Security Conference.

Articles

No US War on Iran: An Open Letter to the UN Security Council

Marco Rubio speech at Munich Security Council

Iran ready for ‘compromises’ on nuclear deal if US lifts sanctions

Trump and Netanyahu align on Iran pressure but split on endgame

BP Optimizes ‘On the Go’ Using Automated Drilling Through MPD

Source: Egyosint on x.com

View

There are 3 things that I see important from last week and going forward through this week and beyond.

US Jobs numbers revisions/CPI.

Iranian rhetoric v Netanyahu collar

US oil production

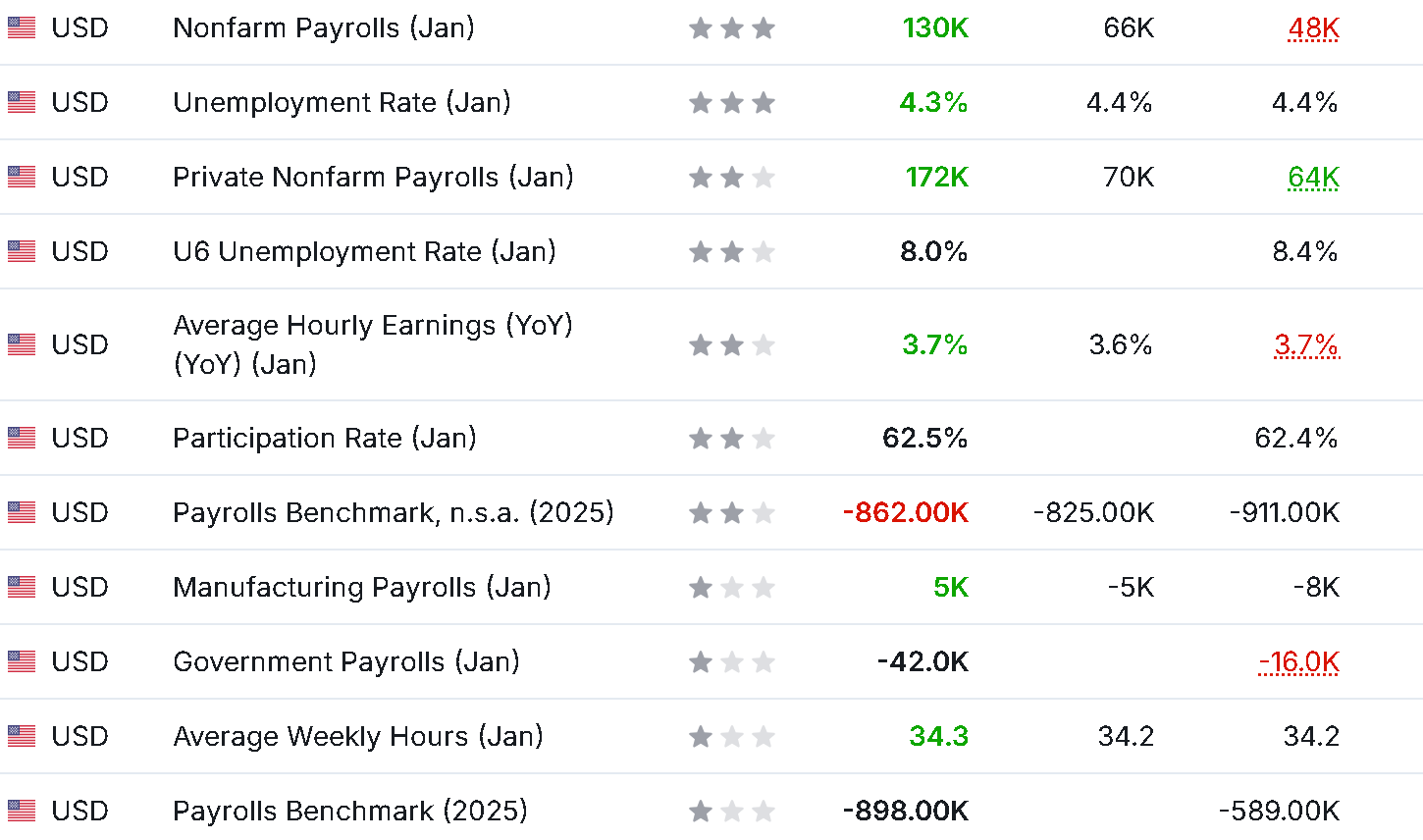

1. The Emperor has no jobs!

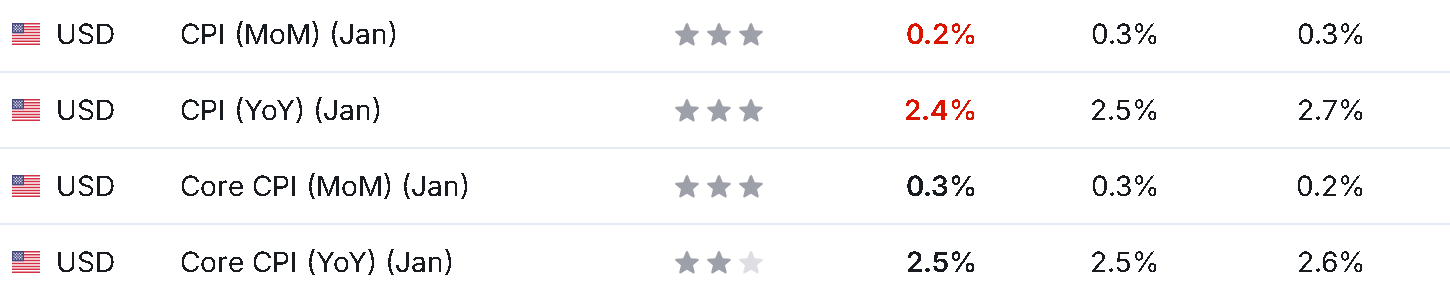

Oil is a great barometer of economics obviously as it is the dominant fuel that underpins shipping, logistics, petrochemical production, transport and pharma. I titled a report 2 weeks ago as ‘There will be inflation’. This was because oil was up 9% on the year. With a forthcoming CPI that would be heavily influential to a fresh incoming Kevin Warsh at The Fed. CPI came out a miss YOY and MOM. So no inflation yet………

Back to August last year, (See ‘Game of numbers’) I have believed that The US administration has been wildly gaming the NFP, Initial jobless and continuing jobless count data. In Q4 2025, the jobs revisions from the BLS was -892k jobs. A massive downward revision, which at the time, sparked a firing of the BLS head by Trump. Last Wednesday we got the late NFP for January 2026 and revisions for 2025. January was a beat of 130k on 70k. A positive number, signalling less expectations for cuts in 2026. However, the 2025 revisions were significant. There was a massive downward revision total nonfarm employment level by 862,000. Total 2025 revised down to +181,000 from the previously estimated +584,000, which is a major reduction in the reported pace of hiring. So they gamed in 403,000 more jobs than actual. Explain to me how you can be wrong by a figure of 403,000 and still be taken seriously? My point here is that this caused a pullback on the US equities markets that infected oil on Thursday and Fridays trade.

Why is this important for oil? Less jobs growth= less productivity= weak oil demand.

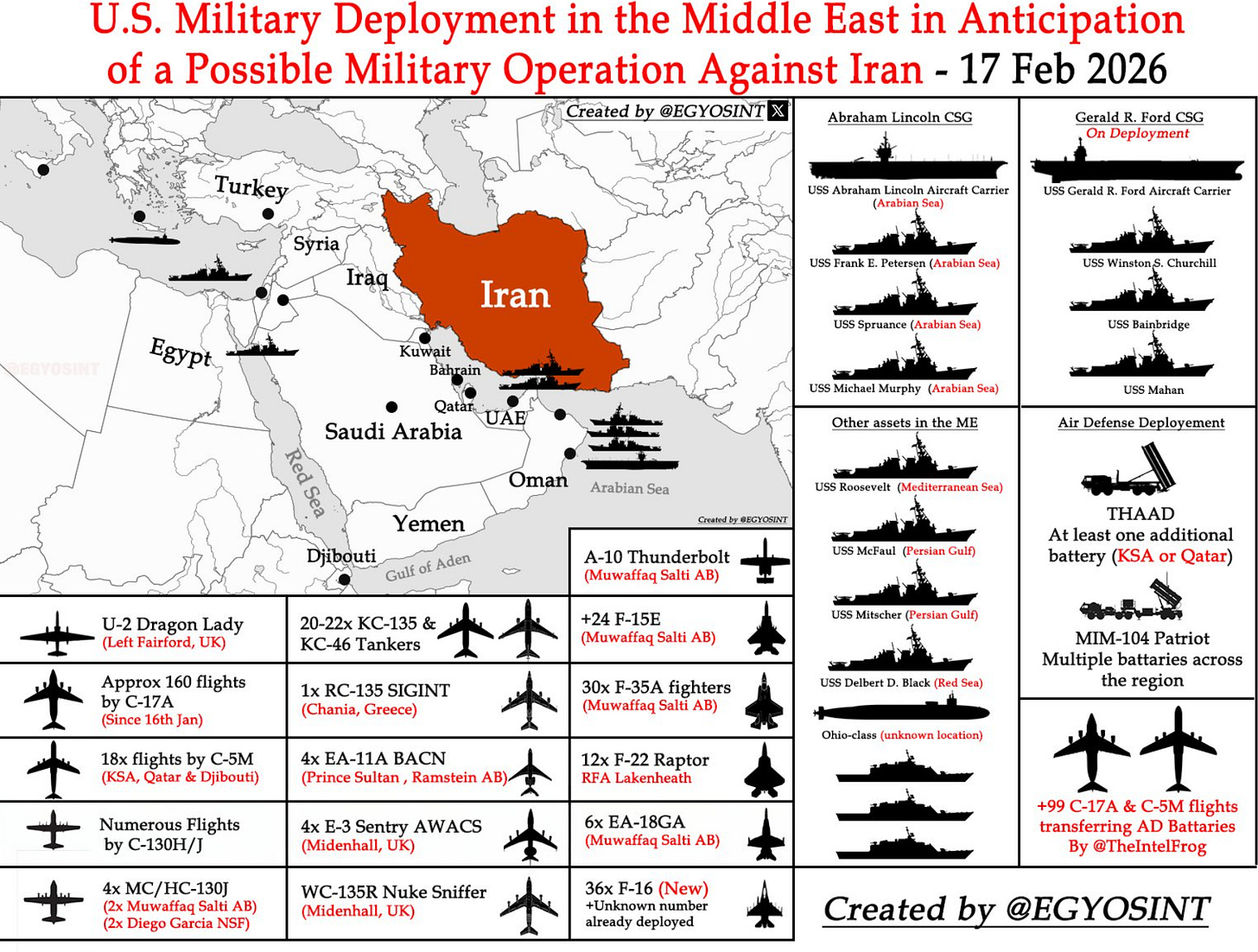

2. Middle East Tensions

It comes as no surprise that Netanyahu is continuing to push for big brother USA into full confrontation against Iran. This was flagged by The Iranian security secretary 2 weeks ago.

It is plain to see that Israeli expansionist ideals reach far beyond their capability in the region. Look no further than the hypersonic Iranian missile barrage on Tel Aviv last June. The impact speed of those Iranian rockets was, as their name suggests, breathtaking and it left the Iron dome system reeling. Netanyahu is hell-bent on creating regional conflicts that they start, but 100% cannot finish.

Price action has been interesting. We started last week holding on to Iranian risk premium, about $64.50. After Wednesdays mixed US labour data (headline good, revisions bad) equities moved lower, dragging oil lower. I am not convinced that oil should be as cheap as it is at these spot levels on Monday $62.50 (WTI 10am Monday 16th Feb). Despite my stated desire to buy a pullback at $60.91- basically too cheap given the macro picture.

Conflict risk premium can not be fully priced out. America is sending a second battle group of ships to the region. This time, Iran are offering to soften on Nuclear talks, should The US soften on oil sanctions. This is extremely unlikely given that US/Israeli talks last week focused on increasing economic sanctions on Iran.

Should that change however, here are the numbers.

Roughly 1.6 mb/d of Iranian crude and condensate exports are currently sanctioned, though much of it still moves primarily to China via a shadow fleet.

Iran is producing around 3.2 mb/d of crude, below its technical capacity.

If sanctions were fully lifted, Iran could likely return 0.8-1.3 mb/d of additional supply within 12 months, potentially pushing output back toward 4.0 mb/d.

So the real risk to additional supply would be a strong addition of 1.6-2mbpd

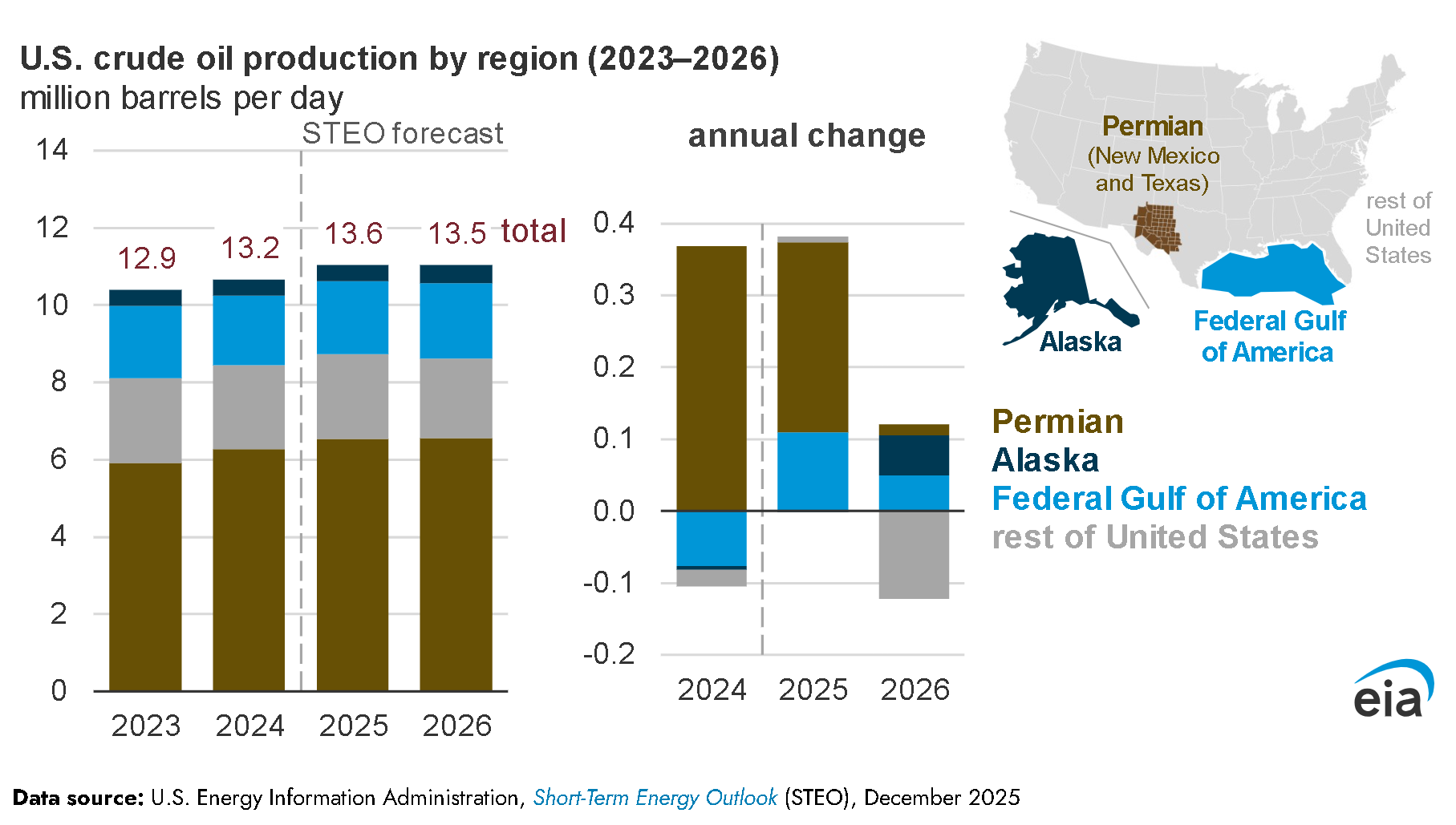

US Production

US Oil production from the lower 48 state has been closely watched since moving into the lofty level of 13.84mbpd last September. In the latest STEO report, it is worth noting that there is a shift in geography taking place for exploration and production. Rest of US production outside of The Gulf/Permian is set to drop completely and move to Alaska. According to The EIA, U.S. crude oil production will average 13.5 million barrels per day (b/d) in 2026, about 100,000 b/d less than in 2025 after a strong 4 years of expanding production.

The only thing that can take production even lower, is lower prices. A few years ago, I invested in an Australian wildcatter 88 energy $88E. I unfortunately did not pull the ripcord fast enough when the market was extremely focused on well logs from an Alaskan site the company was prospecting next door to a Conoco site. I had to average into the gap down and work out on the next pop to minimize losses. Not at all optimal.

There was some oil there, but it was tight and not within their budget to extract. I had to take a haircut on the position. So I’ll be watching this picture from the sidelines because, if 88 cannot get a bid through 26/27, they will NEVER catch a bid.

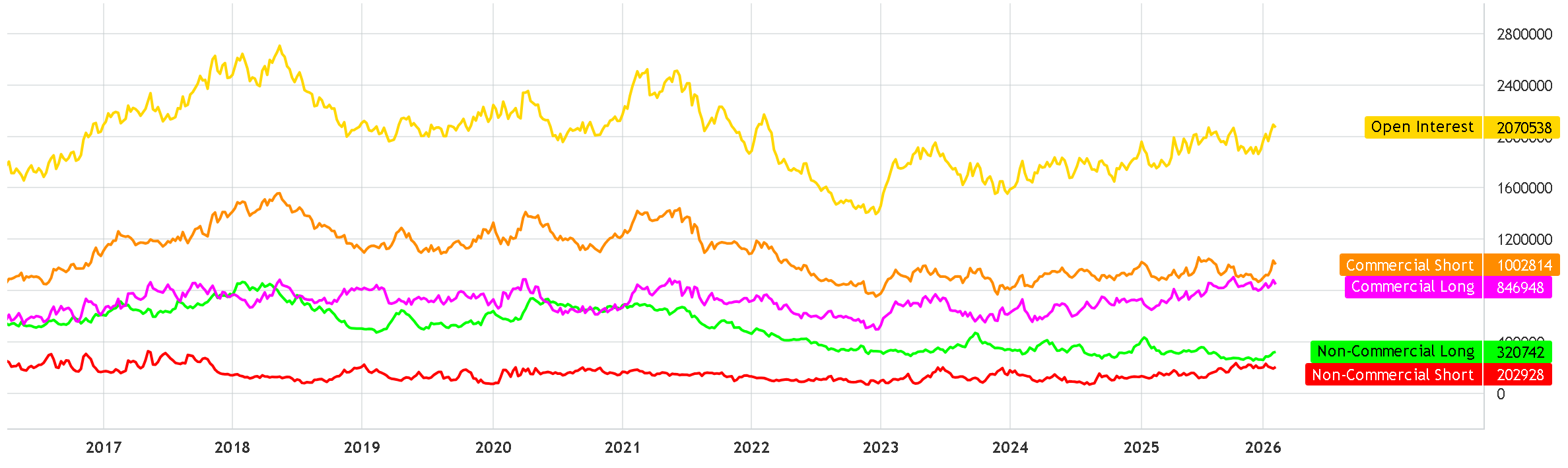

Commitment Of Traders Report

In summary. There are warning signs for short-term bulls if the stretched tops were not enough. Positive signs for medium to long terms bulls.

Open interest -20,776. Total 2,070,538.

Commercials Long -32,984. Total 846,948

Commercial Short -29,617. Total 1,002,814

Non Comm Long +5,213. Total 320,742

Non Comm Short +11,964. Total 202,928.

Flow intensity has decreased WOW- See regime section below. In the prior report, we saw strong hedging via selling from Commercials +76k. As the Iranian risk stalled and price lingered at $64.40s, those commercials reduced that selling forward by 29,617 contracts in the last week up to Tuesday Feb 10th.

My narrative note is that Specs (Non-comms) are building length ie. building long positioning +5,213. Not a huge amount but since Jan 6th, Spec longs have increased from 258,956 to 320,742. This is a 23.86% increase.

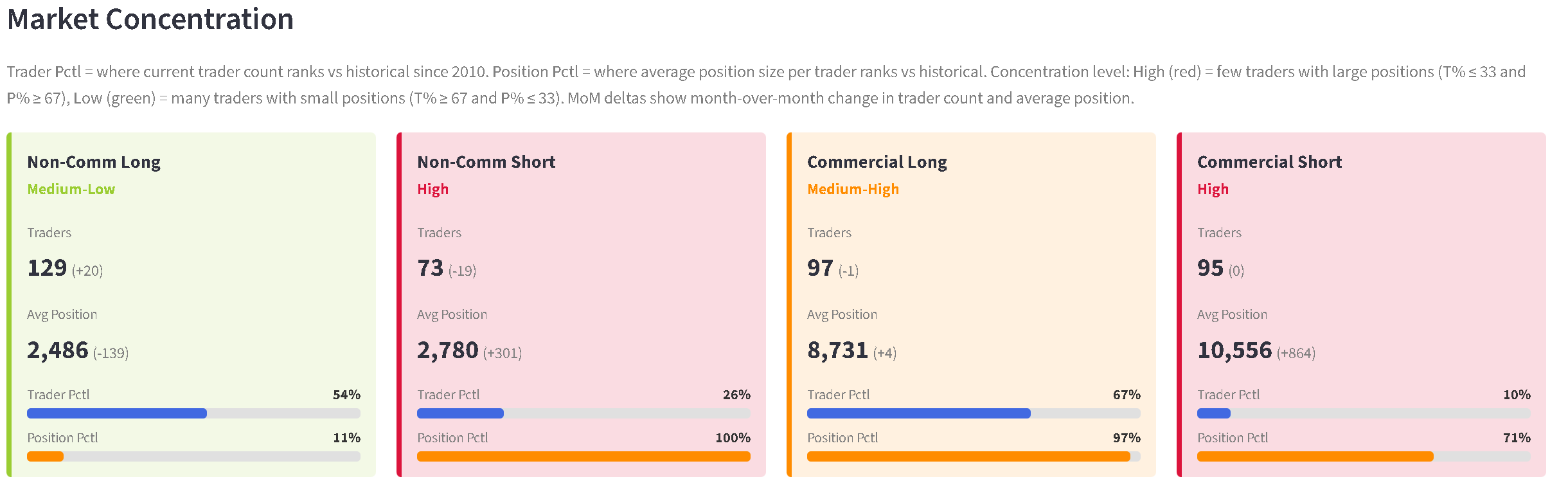

Market Concentration

We see that Non-Comm longs number of traders increased +20, while their average position dropped slightly. On the Non-Comm short side however, where we saw a net increase of +11k contracts while19 traders exited. This tells me that there were still some sellers to get squeezed out, however those that remained saw the highs of the past 2 weeks as a good price to add in more.

Net-net, this has led to a more democratic market and less directional focus than seen last week. I see commercial shorts as being a passive passenger more than a driving influence while we wait for the Iranian situation to take a more defined shape.

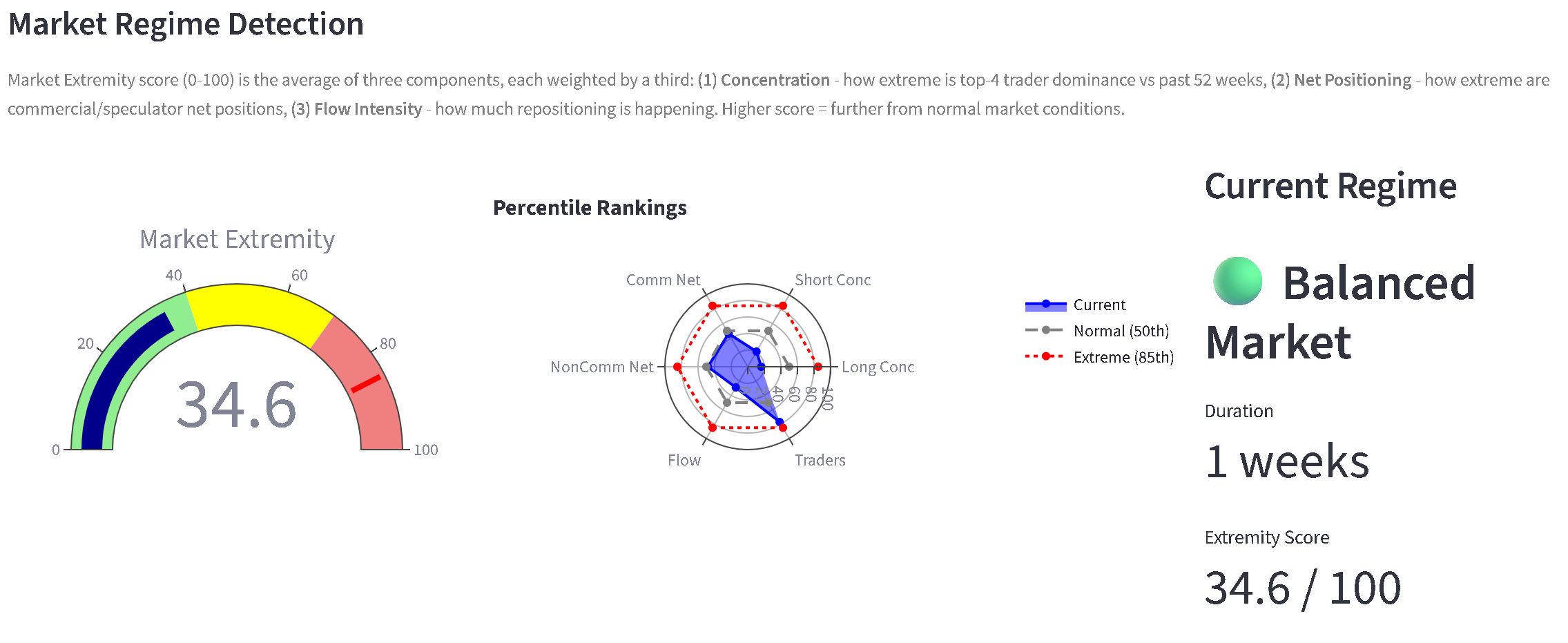

Regime

The regime shifted from last week’s score of 50 back to a more balanced 34.6. This was driven by essentially more Non-comm traders coming in to the market on the long side, balancing out the crowded spec shorts.

Non Commercials/ Specs

Specs stepped off shorts at the end Jan/ Start of Feb. Over this re-elevated Iranian risk, they added to longs significantly last week. This week, we see they sold more on the highs we saw over the last 10 trading sessions, while they also added to longs in a smaller fashion. Net net, there is building going on in the net length on specs.

TRADE

No surprises here, I’m still waiting for $60.91 WTI to buy. As mentioned above, I see Iran escalation/de-escalation as the obvious price driver. Failing any material chance of stance anywhere there, the market is subject to equities market correlation drag.

Should The S&P500 drop 5%, oil would not be able to see refuge from such a deleveraging situation. It is not a comfortable place being a bull in such an environment as the front risks can be wipe-out events if you are over risked.

So net net, there is a lot of sitting on hands.

Trading is waiting. Waiting is trading.