#OUTATIME

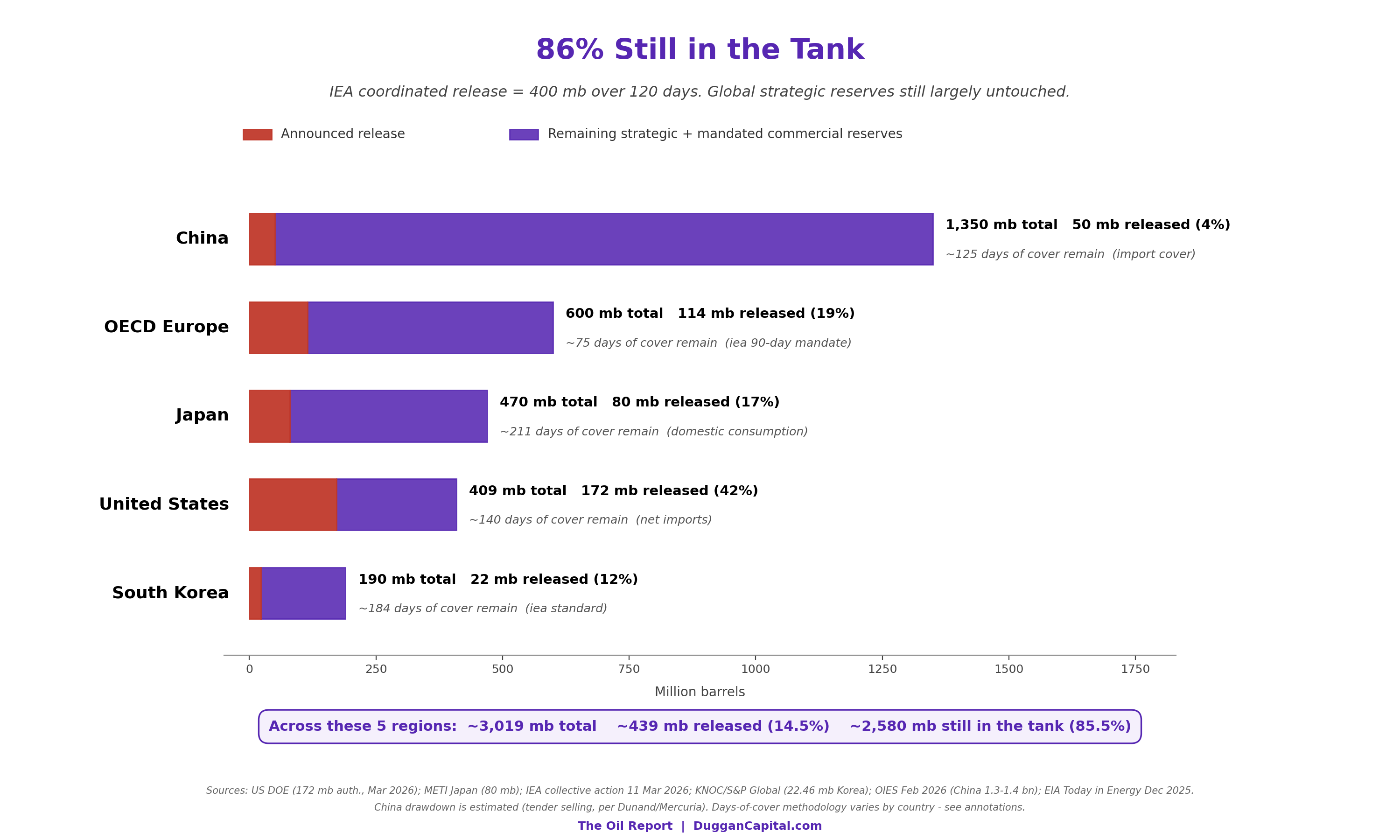

100 days supply left, 120 days to get back to normal.

In this report: Brent is at $101, not $150, for one reason: China is currently a net seller of crude. Mercuria’s CEO says they have about three weeks of inventory left to dump. Thereafter, the world’s largest buyer steps back onto the bid into a market that is already 14.5 million barrels a day short.

Prior week: BRENT+8.13% (+$7.51) for the week. Open $96.12 High $107.40 Low $92.75 Close $99.93

Articles

China “Aggressively” Dumps Oil In Tenders As Iran War Reshapes Flows

Iran deploys more mines in the Strait of Hormuz, sources say

Pentagon dismisses report it could take 6 months to reopen Strait of Hormuz

Trump’s oil export surge — and ceiling

Video: Hormuz Crisis Deepens No Kumbaya

Swiss oil traders anticipate high prices and strong profits

How power markets can adapt to energy crises

(Podcast) Are We Still in the Early Stages of the Commodities Cycle?

Offshore rigs tender axed due to 'unusually steep' rise in day rates, causing frustration

View

Status checks

Countries across the world now working into SPR reserves. On average, the world has at a push approximately 100 days theoretical SPR reserves. See chart in ‘Buffer’ section. Nonetheless, we are started that 100 days last week. The doomsday scenarios everyone is now talking about is this. If the war were to end tomorrow and the SOH were to be open by lunch 100%, it would still, AT BEST, take 120 days to get tankers back to the gulf and then onto their destinations. It would take another 20 days AT BEST, for those now loaded tankers from Hormuz, to get to the likes of Europe or India.

Oh, and by the way, there is a 6-month mine clearance job that needs doing in the SOH.

Trump and Netanyahu have now locked in what will be the most severe energy crisis the world has ever seen. So if Trump and Iran are going to do something, it must be now. More detail on this below in ‘Reality Bites’ section.

Mines

Iran laid a second round of mines in the Strait of Hormuz this week. Trump ordered the US Navy to shoot small boats on sight. And inside the building, the messaging cracked. On Apr 22, a senior DoD official briefed the House Armed Services Committee that full mine clearance would take six months. The Washington Post had the leak that afternoon. Within 24 hours, Pentagon spokesman Sean Parnell publicly called the assessment “an impossibility and completely unacceptable to the Secretary.” The Pentagon is telling Congress six months and telling the cameras it’s impossible. The market is being asked to price one of those two.

The main impact of these mines is that while The Whitehouse wants to carry the line that this will be all back to normal lickety-split, it simply won’t. The mines will take approximately 6 months to clear. This is what we know.

What matters is not the number. It is the fact that Iran can replenish the field at will. US strikes have destroyed 30 mine-laying vessels since the Apr 13 blockade, 16 of them in a single day on Tuesday last. Iran still has scores of Gashti-class small boats, each capable of carrying two to four mines. The DIA’s (Defence Intelligence Agency) 2019 estimate of Iran’s mine stockpile was over 5,000 mines. Fewer than 100 deployed. Less than 2% of inventory in use.

Every clearance timeline the market has been leaning on assumes a terminal count. The Pentagon’s own leaked six-month estimate to the House Armed Services Committee on Apr 22 assumes clearance begins only after the war ends and runs against a fixed set of weapons. A clearance operation that runs concurrently with active re-mining is not clearance. It is maintenance.

The USS George H.W. Bush arrived in CENTCOM on Thursday, the third US carrier in theatre. UK and German mine-clearance vessels are being held back for post-war deployment. Merz: “We could provide mine-clearance vessels. We are good at that.” Nobody is sending them into an active minefield.

The clearance clock cannot start while Iran keeps the strait a live problem. And Iran has no incentive to stop. Yuan-denominated transit tolls are now being deposited in the Iranian central bank. There goes the USD dominance just a little more - read Petro Dollar Protection series. The first revenues have cleared. Every week the strait remains contested is another week of leverage and another week of rent.

The Buffers

The global oil system is now rebalancing with about 8mbpd demand destruction. The situation is contained-despite draws from SPRs around the world. This is the emergency SPRs are built for, and they can hold for another approx 100 days on average. But the real reason oil is trading at $105 instead of $150 is something simpler. China is currently a net seller of crude, not a buyer.

China, selling.

Normal Chinese crude imports run around 11.5 million barrels a day (Dec peak 13.5). Gulf production is currently 12 million barrels a day below pre-war levels, 14,5mbpd per Goldman Sachs. If China is not just absent from the bid but actively putting barrels into the market, the demand side has subtracted roughly the same volume the supply side has lost. That is the arithmetic keeping Brent in the low triple digits.

Vortexa’s latest weekly data shows Chinese onshore crude at 1.3billon barrels. 200 million barrels above year-ago levels. 213 million above the seasonal average. Multi-year highs. China is running down the largest single-owner stockpile in the world rather than replacing it through the tender market.

At the FT Commodities Global Summit in Lausanne last week, Mercuria CEO Marco Dunand told the room that Chinese companies have been “aggressively selling crude oil” into global tenders for the past two to three weeks. OilPrice this week: “China’s Oil Giants Begin Selling Crude as Refinery Cuts Deepen.” A parallel headline the same day: “China Oil Buying Set to Return After Stockpile Drawdown.”

Every one of those data points says the same thing. China is net selling into a market the rest of the world thinks is undersupplied.

The double swing