Rapid Draining

Not your normal demand destruction

In this report: The market is mislabelling a supply shock as demand destruction; the tell is the US redlining at 93% while the world tightens; genuine destruction is narrow (jet, petrochem); inventories are draining at a record pace toward a record OECD low by end-May. The pain trade has been longs, now its the shorts.

"9 mb of the 11 mb of US SPR crude exported so far were shipped to Europe." Source: IEA citing Kpler shiptracking

Articles

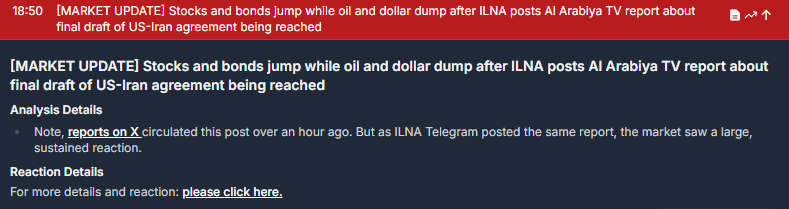

Spokesman: Iran, US Edge Closer to Finalizing MoU

No full Hormuz flows until first half of 2027, UAE’s oil giant says

What Does Demand Destruction Mean for Downstream Oil and Gas?

Emerging consensus suggests oil to remain capped near $100 over next year

NATO is starting to consider Hormuz mission to protect ships

China and Climate: China Restricts Fuel Exports, Solar Exports Surge

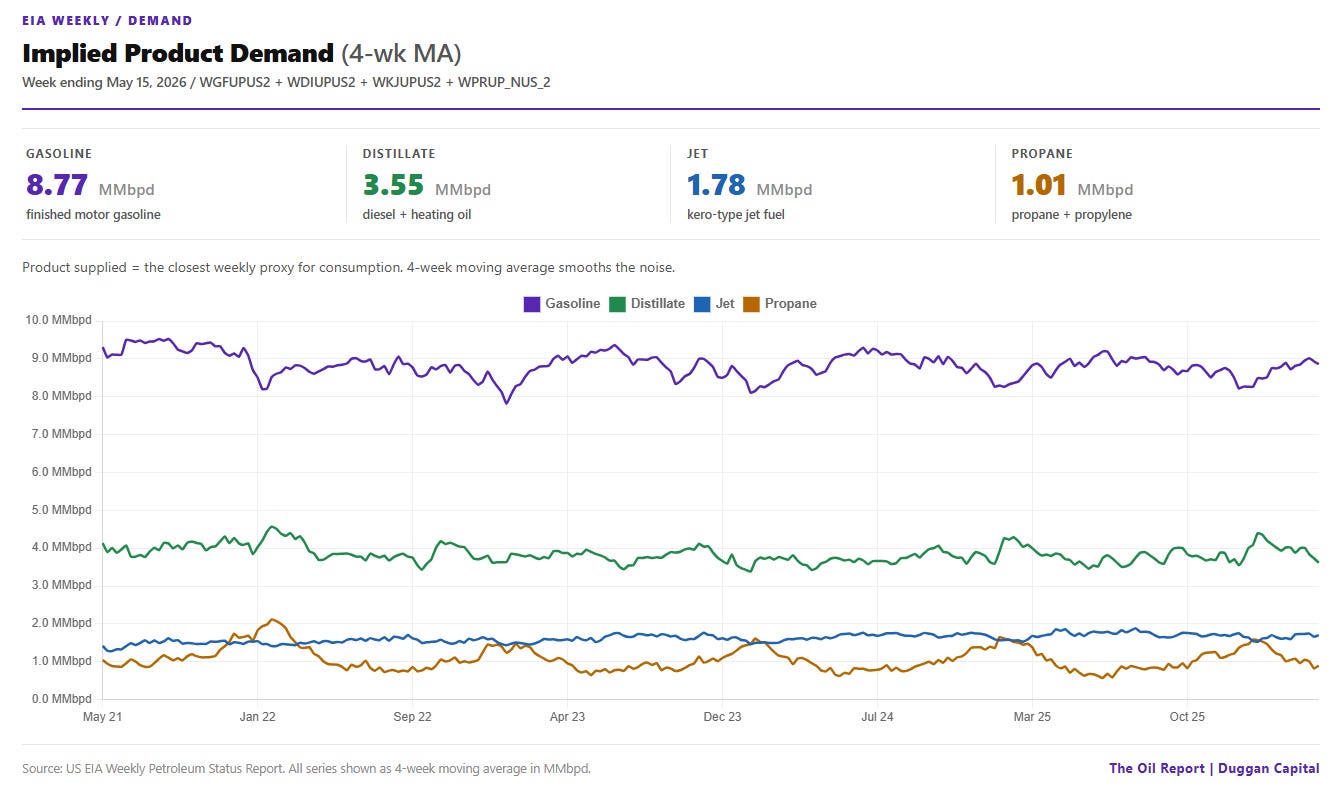

The Oil Report weekly EIA data book.

The US downstream system running in max-output mode

New Iran peace proposal triggers tense Trump-Netanyahu call

Hormuz traffic edges higher after lull

View

Just quickly, here is the note I put out regarding this new ‘peace deal done’ headline last night. It is more of the same - Trump front-running negotiations. There is no new ground on nuclear or sanctions negotiations. They are closer, but no cigar yet.

Lets move on.

There are two fears in this market right now, and both are real enough to move price. The first is behavioural: that high prices have started to destroy demand. The second is physical: at the current rate of draw, the world’s oil stocks are racing toward “tank bottoms” by the third quarter.

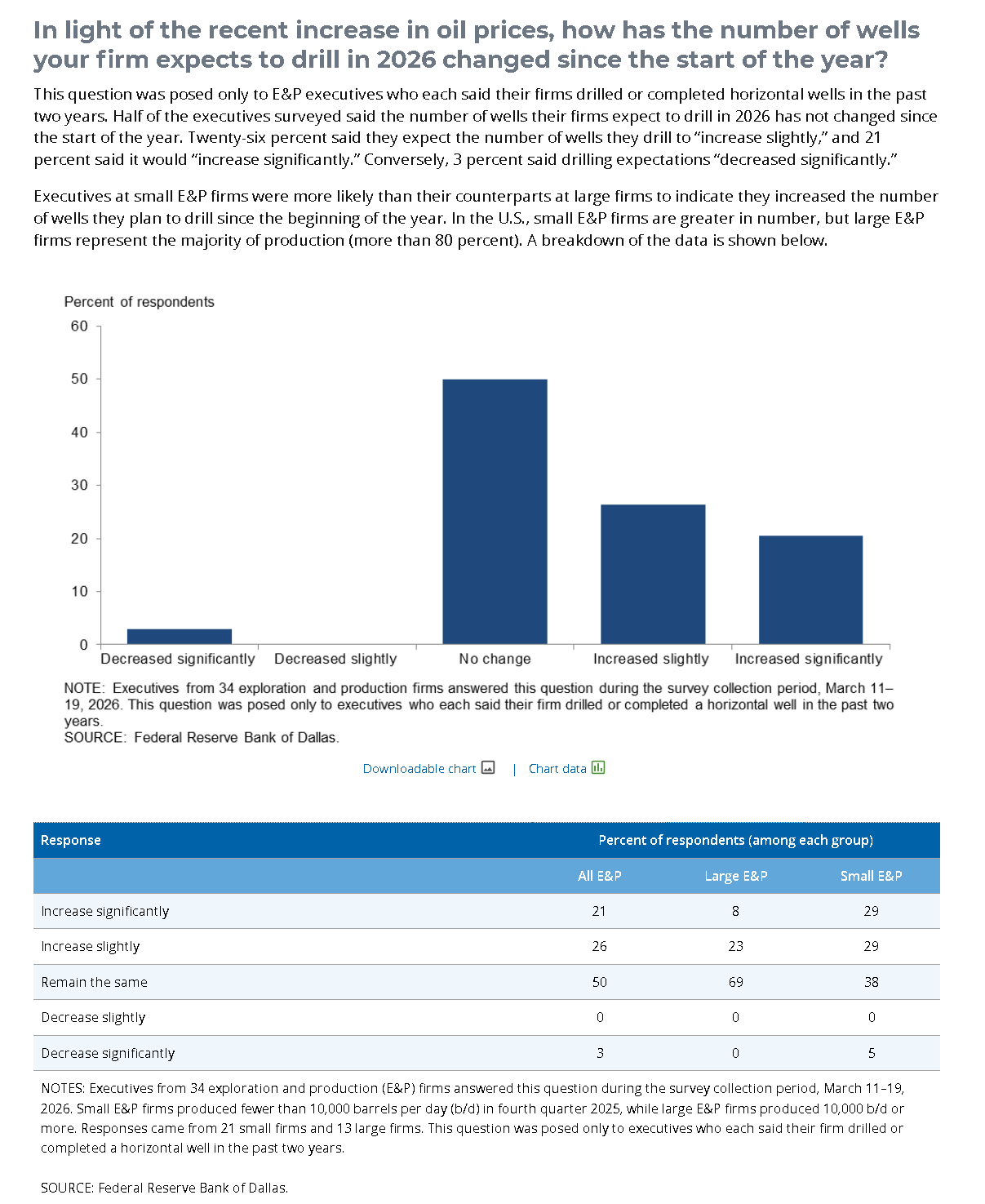

We are in the new medium-term normal now (The New Normal, 11 May): the Strait of Hormuz is gated and tolled, and the industry is slowly reorganising around it. The US is cast as the world’s swing producer, (having taken over this role from Saudi Arabia a few years ago), but only if its shale answers. The Dallas Fed says half the US drillers will, but currently, we have rig counts slipping at $100 WTI and $66 break-evens ignored. (Read Cap Ex Baby, Cap Ex, Dec 2024). There is no grand peace deal that resets 2026, and on the horizon the market is actually pricing, no reset at all. Welcome to the new world where Drill Baby Drill might actually happen!

Demand destruction

Demand destruction means one thing: consumers changing behaviour permanently, not returning to old habits even when prices fall. By that measure, most of what is being called demand destruction right now does not qualify.

The tell is in the refinery data. Asia’s runs fell 2.7 Mb/d in March because the feedstock stopped arriving, crude imports at a 2016 low. Europe’s jet imports are running 60% below last year not because European airports went quiet, but because the Gulf stopped exporting. This is supply-side rationing wearing a demand mask.

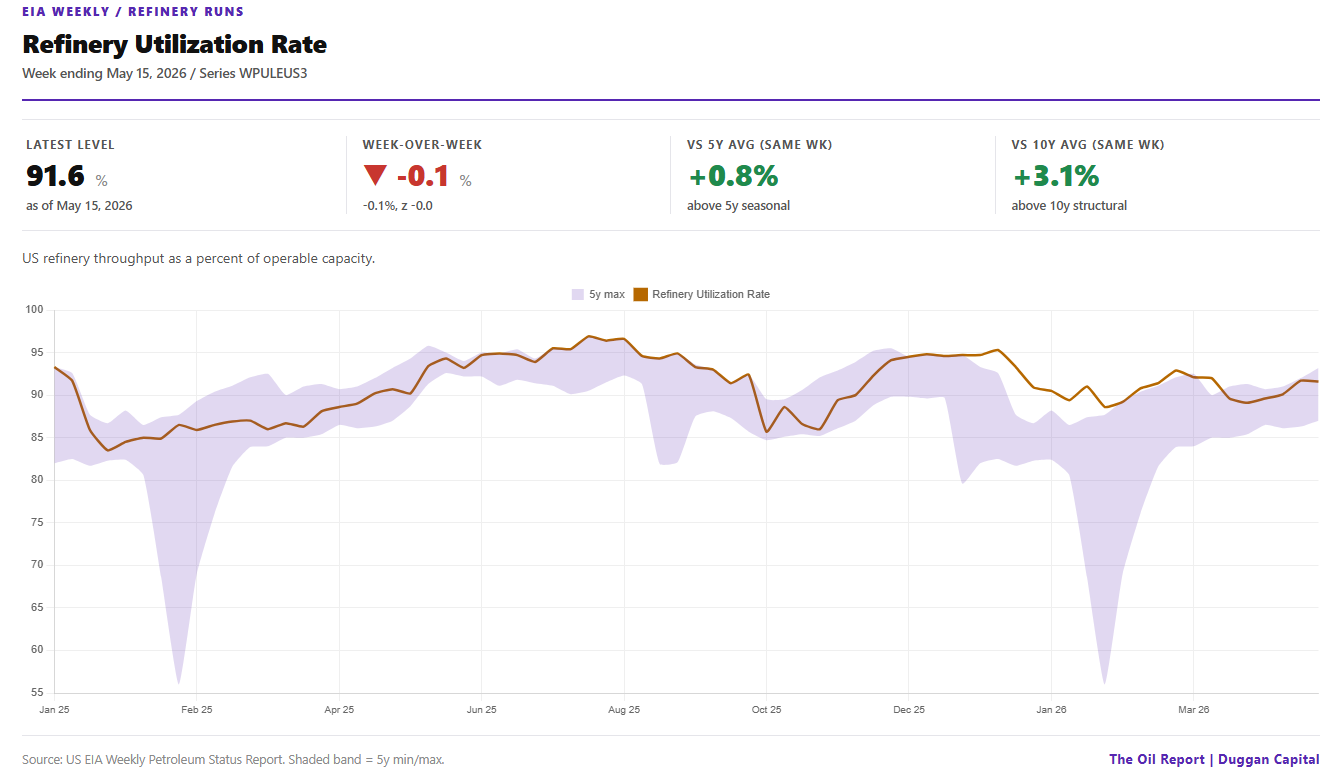

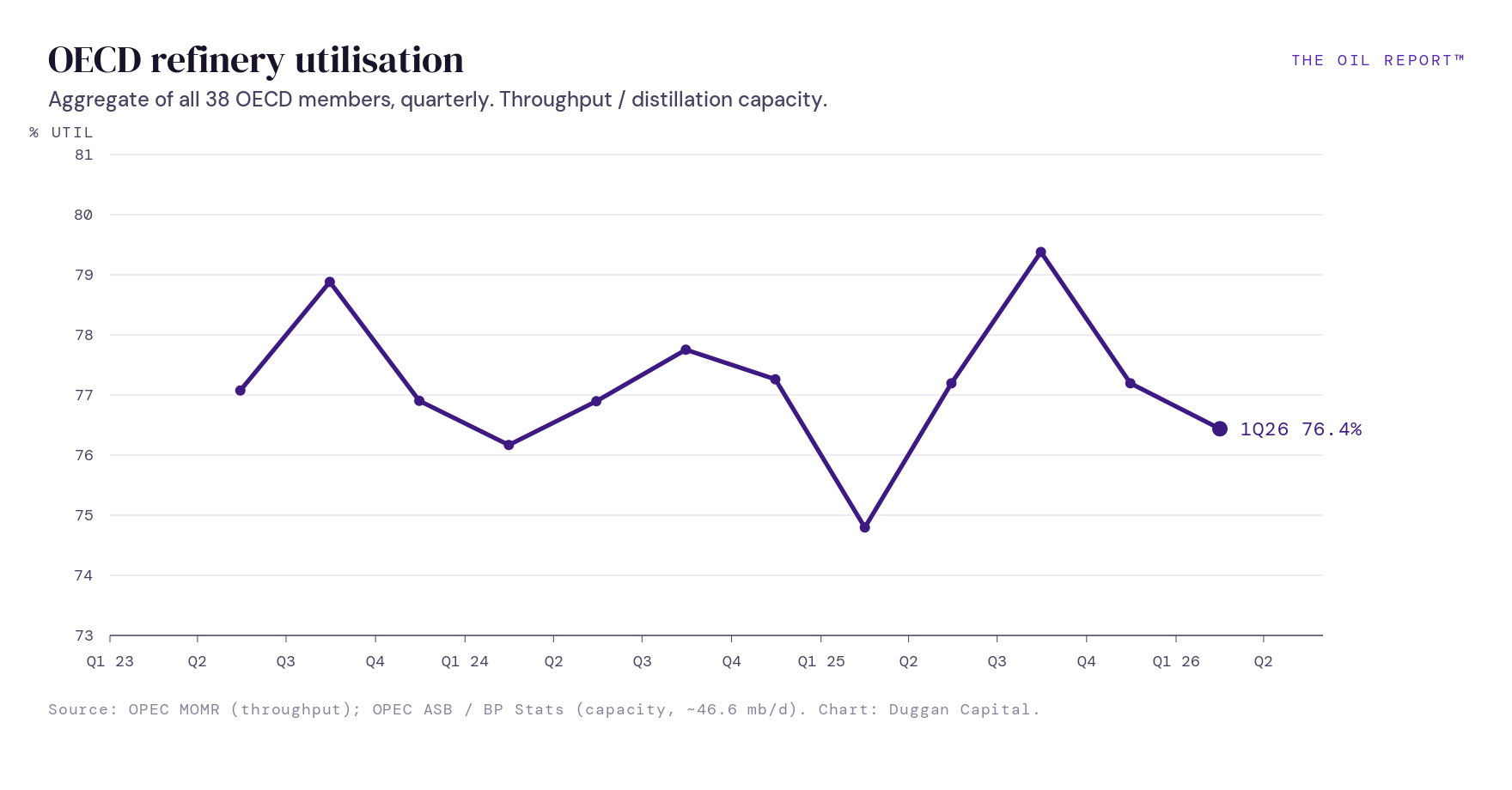

The US refinery data is the contradiction. If demand were dying, the world’s marginal refiner would not be running at 93% utilisation. It would not be posting record product exports of 3.3 Mb/d. And its domestic product stocks would not be hitting five-year lows.

The US is running hot for two reasons, and they are different barrels. On the product side, margins of $24-31/bbl on the Gulf Coast are pulling throughput to 93% while record product exports drain domestic stocks to five-year lows. On the crude side, Washington has separately released around 31 mb from the SPR since early May, much of it going straight to allies in Europe. The backstop is bleeding from both ends.

To be clear: demand destruction is happening, just not everywhere. Aviation is the most obvious case, with global passenger kilometres falling year-on-year in March for the first time in five years. Jet fuel was the first product to go. Petrochemical feedstocks are contracting at depths last seen in the 2008-09 financial crisis. These are real.

The broader demand destruction talk is, for now, a mirage. It suggests the market self-corrects as consumption falls. What it is actually doing is forcing people to seriously consider the alternatives. Solar panels. EVs. Hybrids. That structural shift is real and it is accelerating. So its a supply led (rather than price) demand destruction.

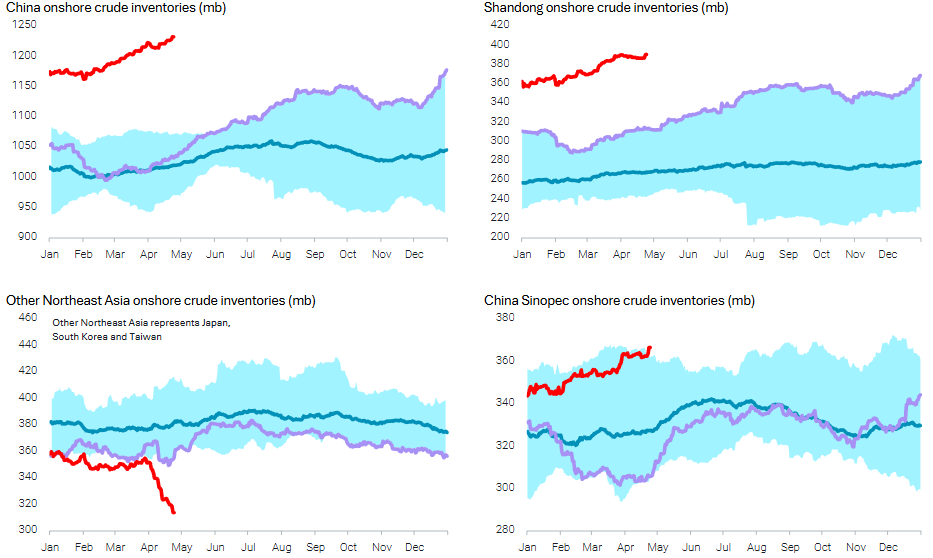

China is the one case that does not resolve easily as the largest buyer. Seaborne imports and domestic fuel sales are both down. But onshore crude inventories are up 15% year-on-year and sitting near record highs. That looks less like a market running out of demand and more like a well-stocked buyer choosing not to import. It is the one I am watching most closely.

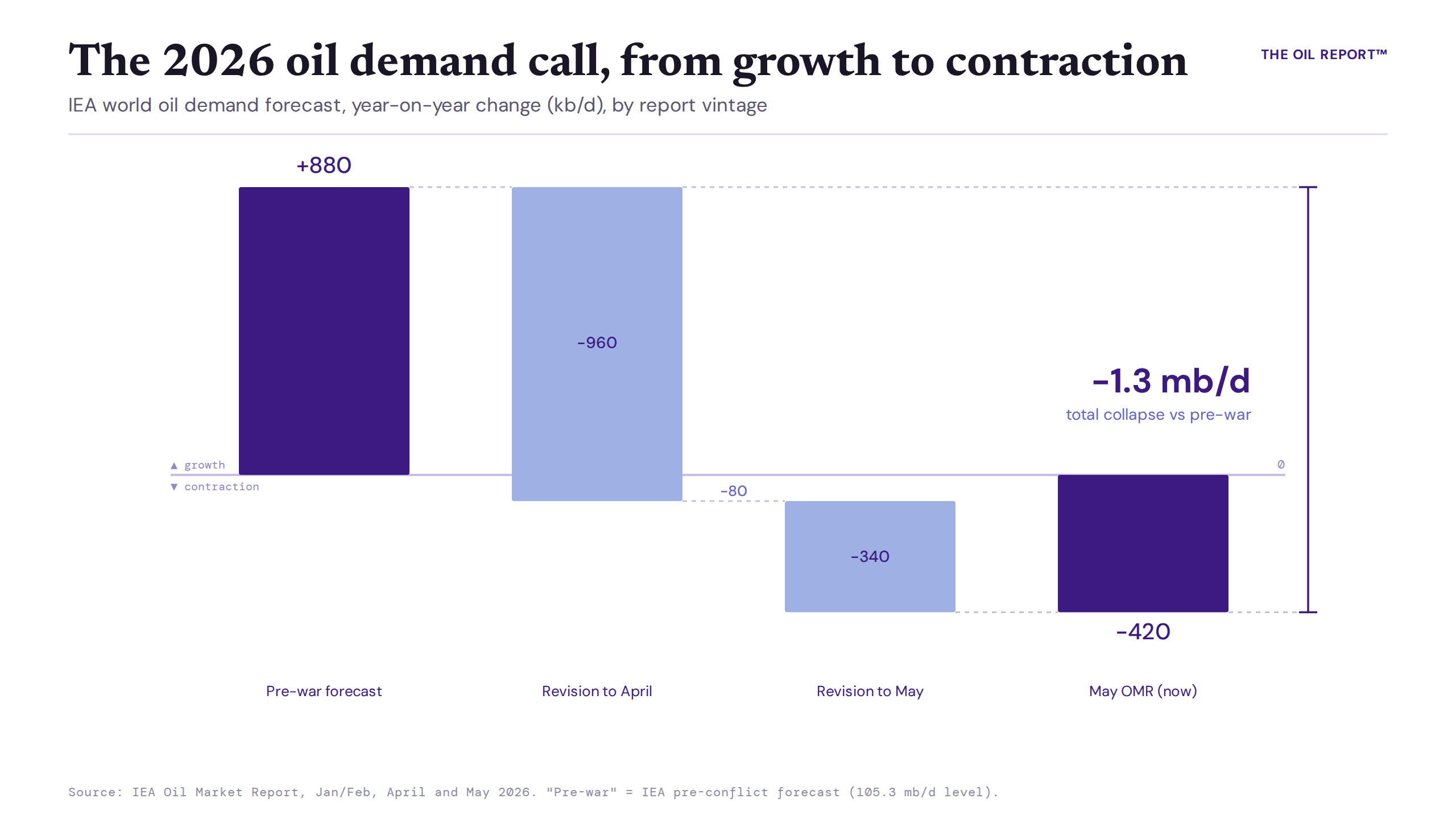

The obvious pushback is that demand will rebound. The EIA agrees, already pricing in a 1.5 Mb/d demand recovery in 2027 once supply flows resume in some way, shape or form. If it all comes back that cleanly, it was never destroyed. It was rationed. Essentially, what China has decided to do. The existing measures include export halts on refined fuels, production quotas and price caps and subsidies.

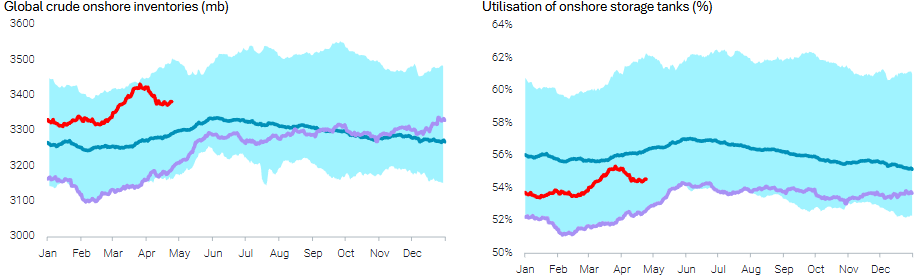

Inventories

If demand is not the relief valve, inventories are. And they are running off a cliff. See below

Keep reading with a 7-day free trial

Subscribe to The Oil Report to keep reading this post and get 7 days of free access to the full post archives.