The NACHO trade

Not a Chance Hormuz Opens

In this report: J.P. Morgan's September inventory floor. The UAE walks. Kuwait exports zero. Europe's gas math is one warm summer from breaking. Iran's 13-point proposal versus Trump's blockade prep. Commitment of traders analysis and expanded trade section.

BRENT Last week +4.65% (+$5.11) for the week. Open $106.60 High $115.30 Low $105.55 Close $114.31

Articles

UAE quits OPEC: What that means for the Gulf, energy markets and beyond

China Orders Refiners to Ignore U.S. Sanctions on Key Iranian Oil Buyers

Trump orders aides to prepare for extended blockade on Iran — as Tehran’s economy collapses

Oil could trade at nearly $120 if war drags on, Goldman Sachs warns

Trump-approved pipeline could increase Canada-U.S. oil exports to 1M barrels per day, expert says

Legendary Trader Paul Tudor Jones on AI Risk, Bubbles and Buffet

Egypt advances alternative Europe

DOE has released 17.5 million barrels from the Strategic Petroleum Reserve since

View

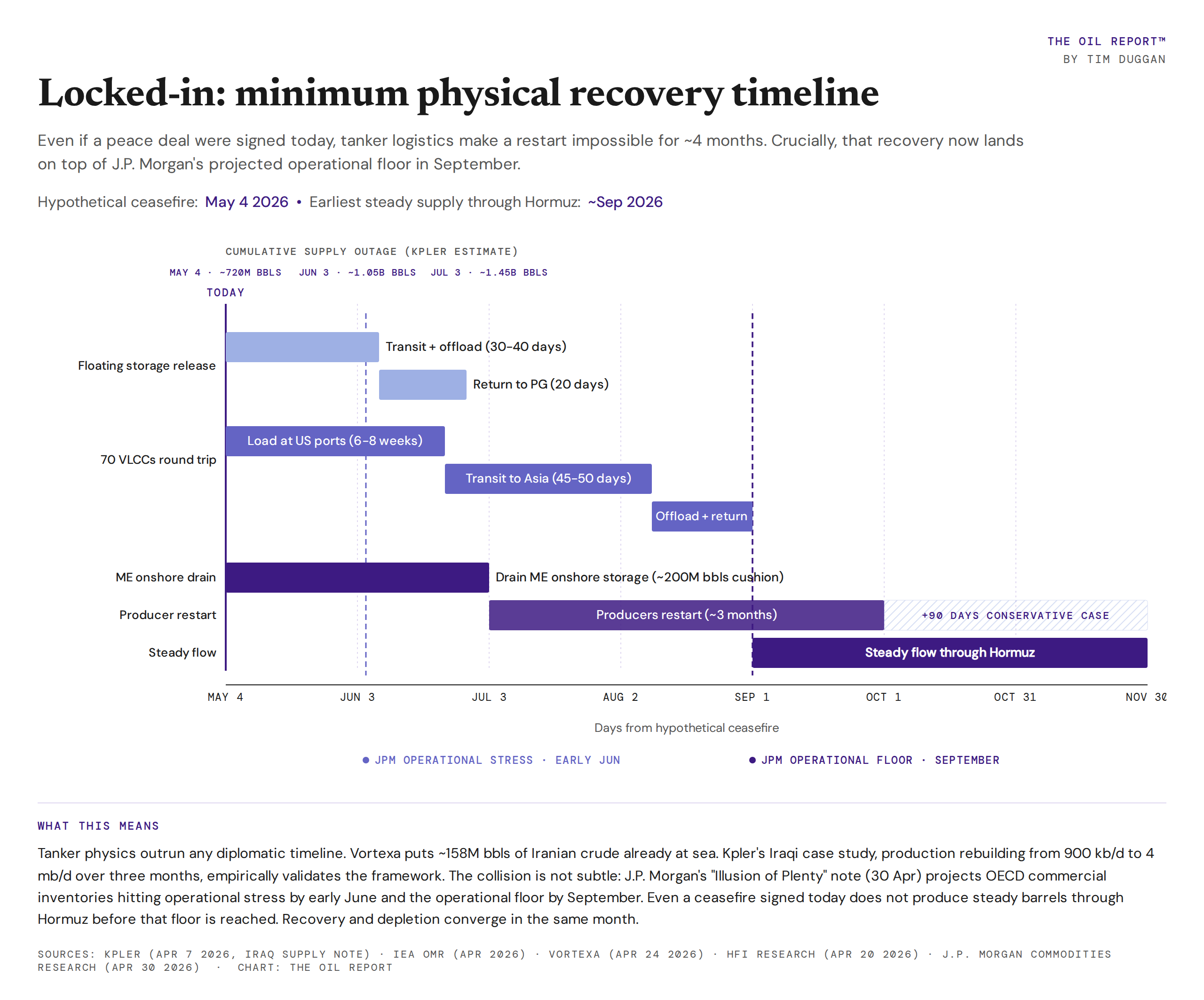

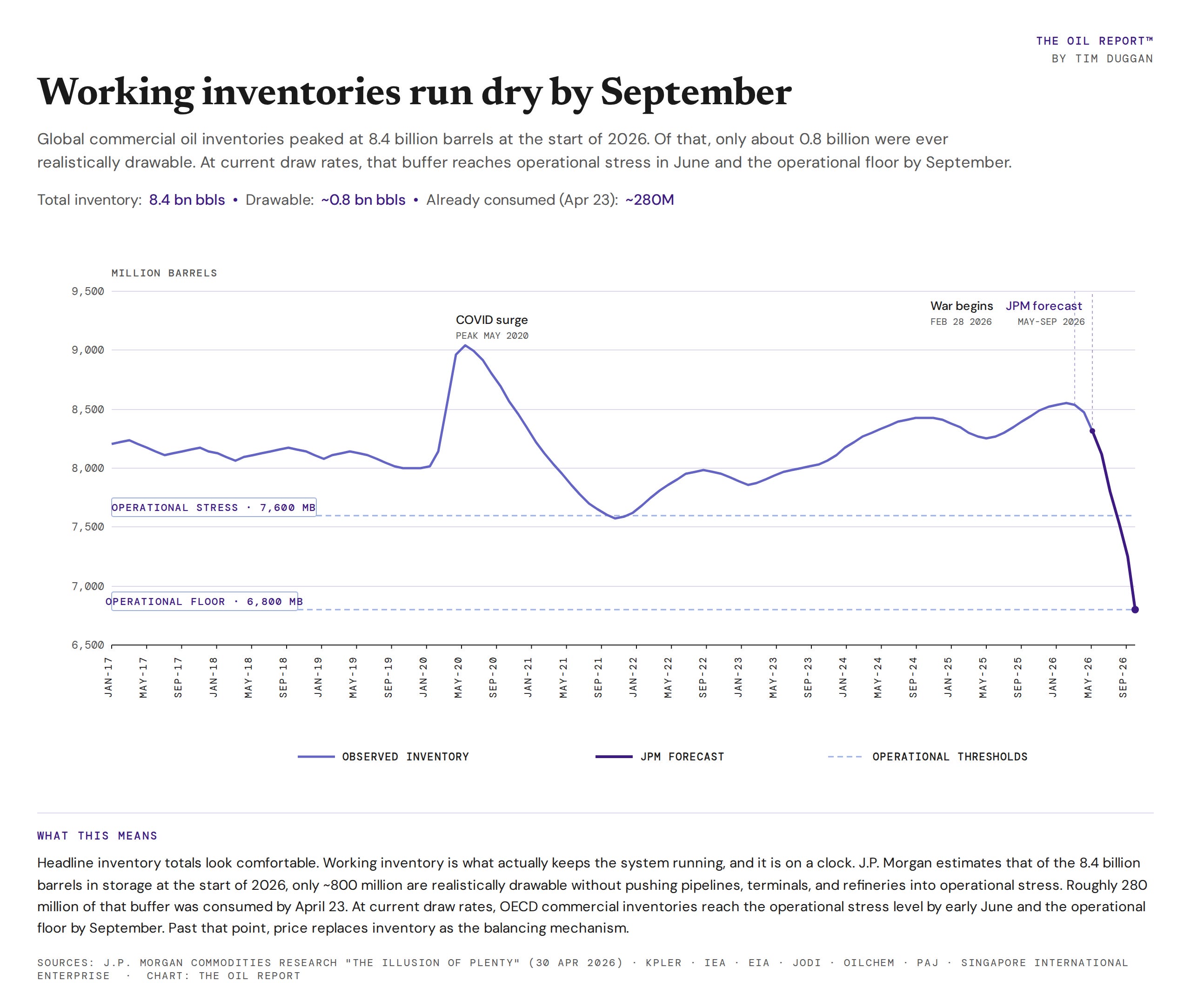

As I talked about in several previous reports to date, we have entered into an energy timeline that terminates in September. The cracks will become critical in roughly 4 weeks from today. This is elegantly drawn out by J.P.Morgans Natasha Kaneva in a private client letter last week titled ‘The illusion of plenty’. To summarize, the world holds 8.4 billion barrels of oil in storage. Only 0.8 billion of those are actually drawable, and at the current pace of withdrawal, OECD commercial stocks reach operational stress in June and the operational floor by September.

What is coming isn't fully priced in. We have not seen the whites of the situation’s eyes yet. And we will in 4 weeks. We will see new higher highs on oil, be it on forties physical or on paper futures. Either way, this tepid, almost controlled market will not last- and yes, it is tepid. The world has grown accustomed to the less violent face of oil price action. We forget this market can do everything you think it can’t do.

As a business operator and family man, I want to be mindful of what I should be doing today, in order to react to the market in 4 to 8 weeks time. We need to be asking ourselves the question of what does my business look like at the end of June, what stress scenario can I take in September? What do I do in a 30% higher energy environment? If this was equity markets, I would be talking about a temporary ‘blip and dip’ scenario. This is not that. This is energy markets. This is diesel and petrol in your car, gas you cook with, bunker fuel that powers shipping tankers, fuel that powers your logistic chains. Where the stock market is not the economy. Energy access and price is the economy.

Saudi Arabia and Friends

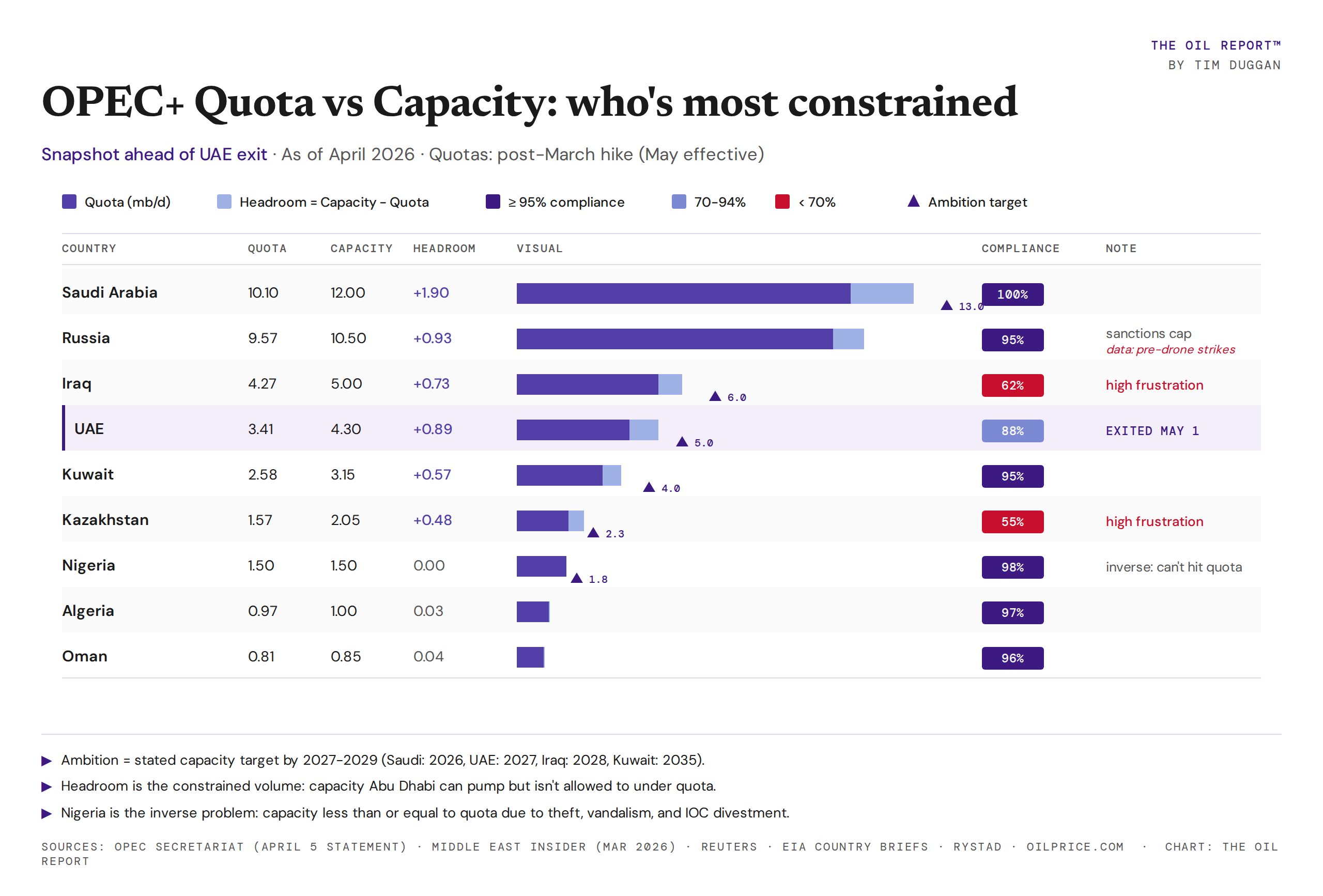

The UAE is OUT of OPEC. Done.

The UAE produced 3.42mbd in February 2026, 11.9% of OPEC's 28.63mbd total. Lying third being Saudi #1 10mbd and Iraq 4mbd. In short, they left as they were constrained by production quotas that had haunted the relationship going back to the post COVID-19 landscape. They have ambitions to produce up to 5mbd from current 3.4mbd. Remaining in the group would constrain those growth targets and thus their GDP. FYI Kuwait just went to zero oil exports for the first time ever.

Until they left, they had only made 88% compliance, quietly producing about 190 kb/d above quota. The list of the bad boys of OPEC+ is Kazakhstan 430 kb/d above, Iraq 130 kb/d above, Russia 150-450 kb/d above.

There is a lot of further talk of more dissent, with little evidence. The chatter is entirely based on the fractious nature of this Iran crisis. One member country (Iran) attacking another member country is bound to lead to a bust up at the annual Christmas dinner. But with Iran remaining in the group producing 3.4mbd others may also look to leave. See table below. This is only the list of OPEC+ countries that are constrained by the quotas’ mechanism agreement. OPEC & OPEC+ totals 22 countries in all.

European gas

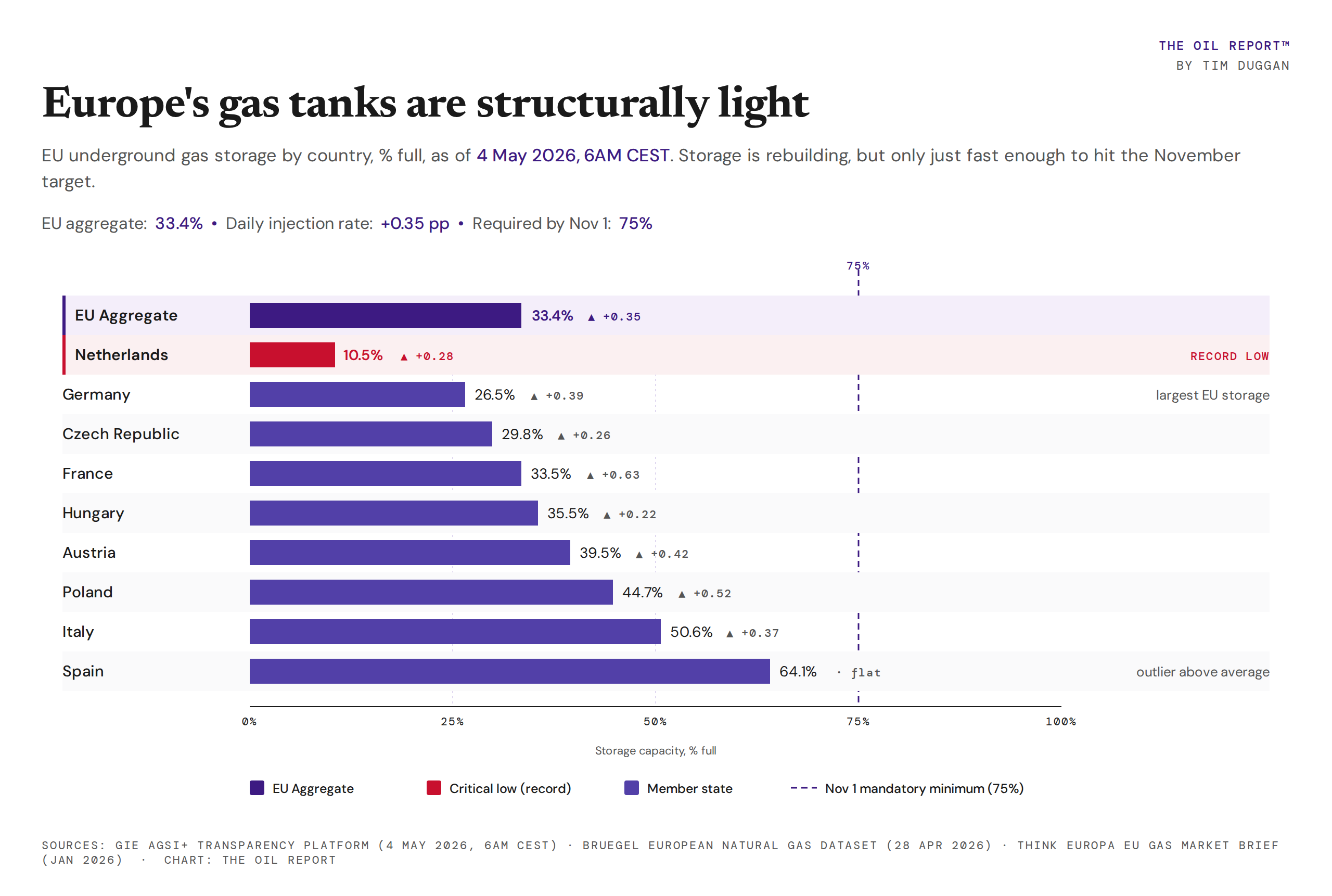

The EU is sitting at 33.4% on May 4. To reach the 75% mandatory minimum by November 1, member states need to inject at +0.23 percentage points per day for the next six months. Current daily rate: +0.35. The math works, and only because Brussels lowered the binding minimum from 90% to 75% in September 2025.

Netherlands at 10.5% is the structural alarm, sitting at the lowest stored level on record for the start of the injection season. Spain at 64% is the outlier, propped up by Algerian pipeline gas that does not flow through Hormuz. Every other major economy is more than 15 percentage points below where it would normally sit at this point in the year.

There is no margin if anything goes wrong: a hot Asian summer pulling LNG cargoes east, an early winter, or any further disruption to Qatari flows.

Everyone’s got a plan

Iran put forward a 13point plan with 3 phases. Tehran’s new proposal came in response to a Washington-backed nine-point peace proposal, which primarily sought a two-month ceasefire. However, in its latest peace proposal, Iran said it wants to focus on ending the war instead of extending the truce and wants all issues resolved within 30 days. This is good material talk from Iran. There is hope! As I mentioned before, this war ends when Iran decide, not The US.

The new proposal calls for

guarantees against future attacks

a withdrawal of US forces from around Iran,

the release of frozen Iranian assets worth billions of dollars and the lifting of sanctions,

war reparations,

ending all hostilities, including in Lebanon, and

“a new mechanism for the Strait of Hormuz”

Iran is now materially coming to the table. It would be presumed that we are then within a 14 day sight of potential agreements; however, we have been here several times in US/Iran negotiations. The difference here is that Israel may be sidelined and forced into de-escalation. To date, they have not adhered to US orders to step down. Adding to the entire picture is the reported ill health of Netanyahu. Add to this, Bessant’s comments that the US blockade may last ‘‘months if needed.’’

There will be a lot of noise about Iran’s railway route to China. This really is a non factor. The pre-war capacity was 1.8mbd, however the railway is damaged and overland capacity for Iran is a small 250k-300 kb/d.