There will be inflation

Landings increase while Iranian risk prices

In this report: Where the Iranian risk premium is the upside whip, increasing onshore storage is the downside lash!

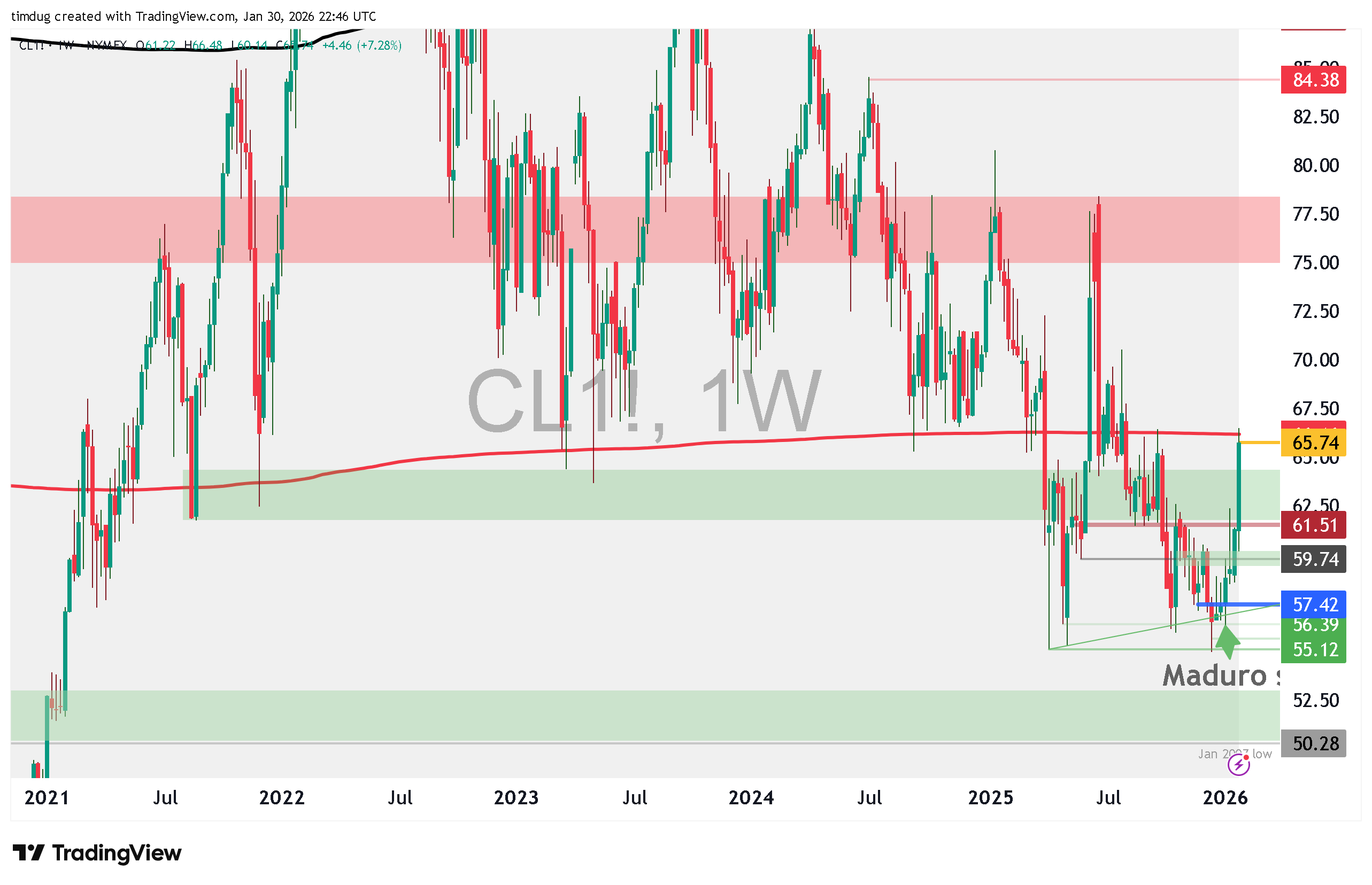

Key Stats. WTI +7.28% (+$4.46) for the week. Open $61.22 High $66.48 Low $60.14 Close $65.74

This was the result of oil trading on guidance as of last Sunday. Tuesday delivered entry into the prime long execution zone—after that, the market never looked back. Thank you for your attention on this matter. :)

Articles

What could happen if the US strikes Iran? Here are seven scenarios

OPEC+ set to keep oil production pause for March as prices jump, sources say

Marginal cost of U.S. shale to move from $70 to $95 WTI by mid-2030s

Some notable squawk from the week from the boys at Newsquawk.com

View

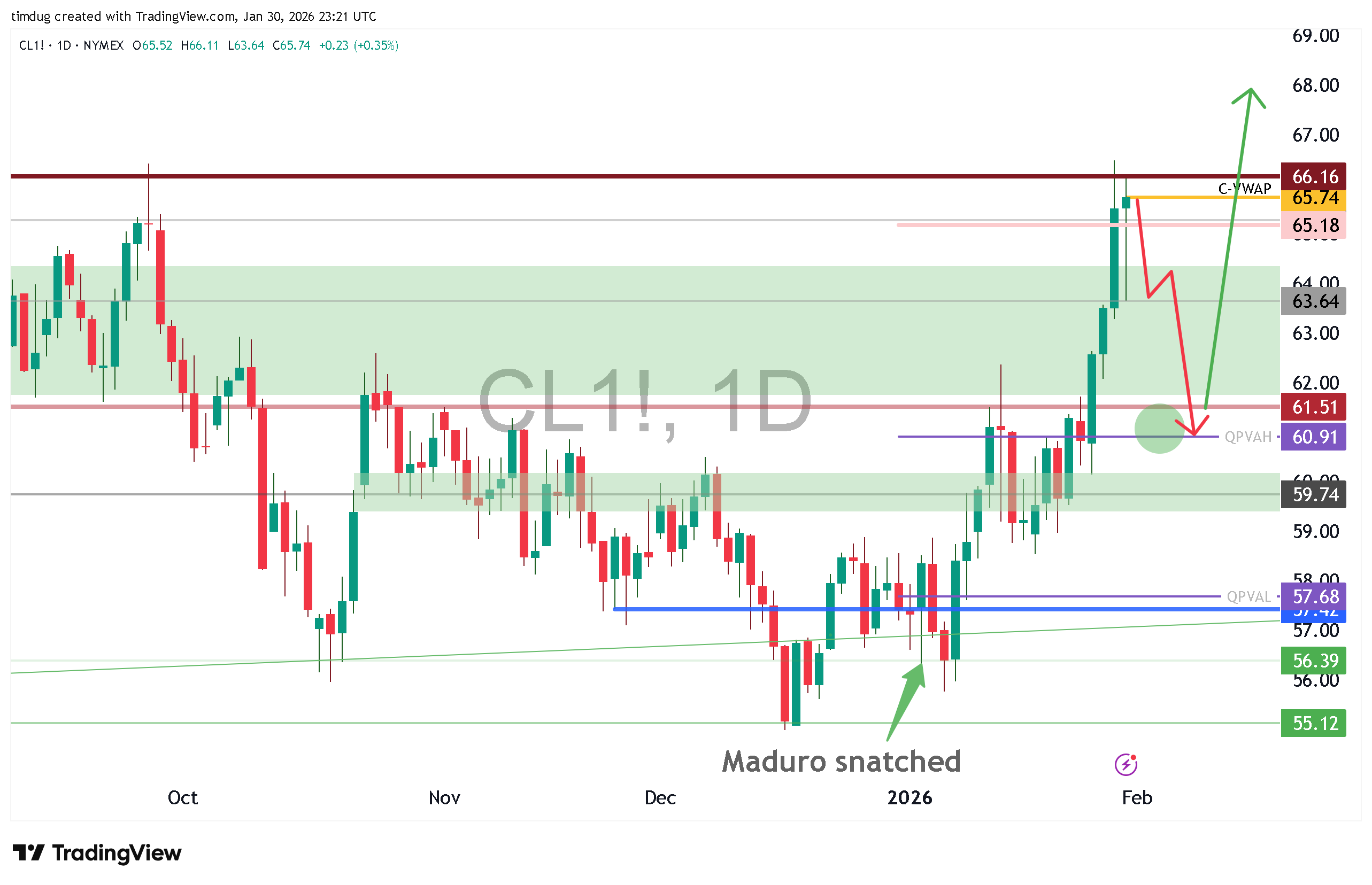

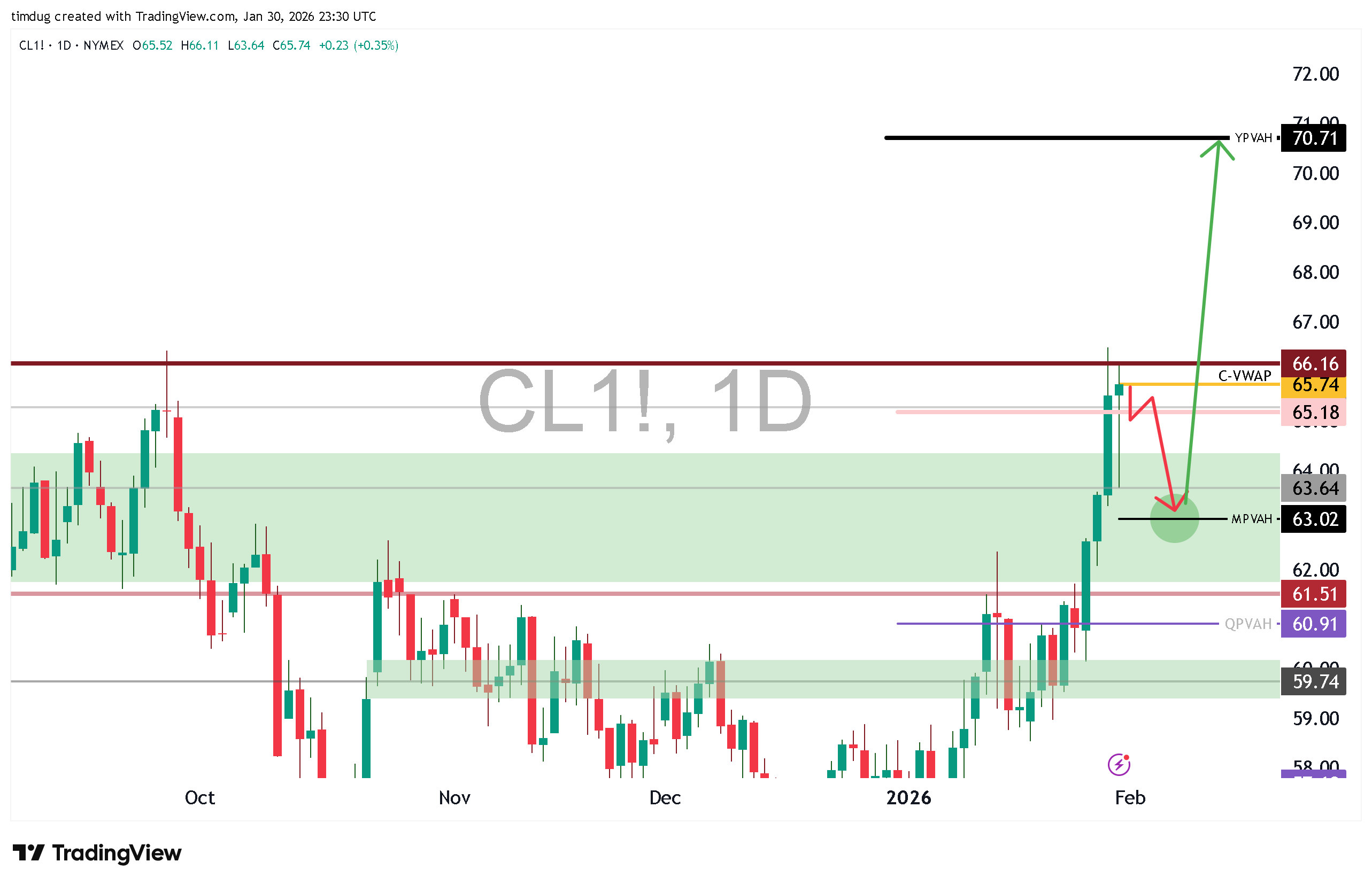

The glut narrative is sailing off into the sunset, leaving commentators and speculators kicking around the now dead chatter. If your CTA is still afraid of the glut, he is behind the information curve. The crude is still there to a large degree, just now diminishing, along with Specs hopes of tipping oil prices well below breakevens. It wasn’t enough, and from the Maduro snatch, where people were calling for gap downs to $52, the market moved up 16%/ $9 in their face. This event served as a large clarity check for the market-between those who bothered to understand Venezuelan oil, and those that trade headlines and news.

Venezuelan production was never going to ramp up in under 2 years, regardless of how much money would be invested. Added to which, the diluent factor is large. Every barrel of oil from Venezuela (Orinoco grade- a super heavy crude) requires 0.3 barrels of Lighter grade WTI, naphtha or condensate to make it transportable and work in refinery. Its more like a tar than anything and has to be watered down in order to flow. Also referred to as a non-Newtonian fluid.

Then 4 days later again…..

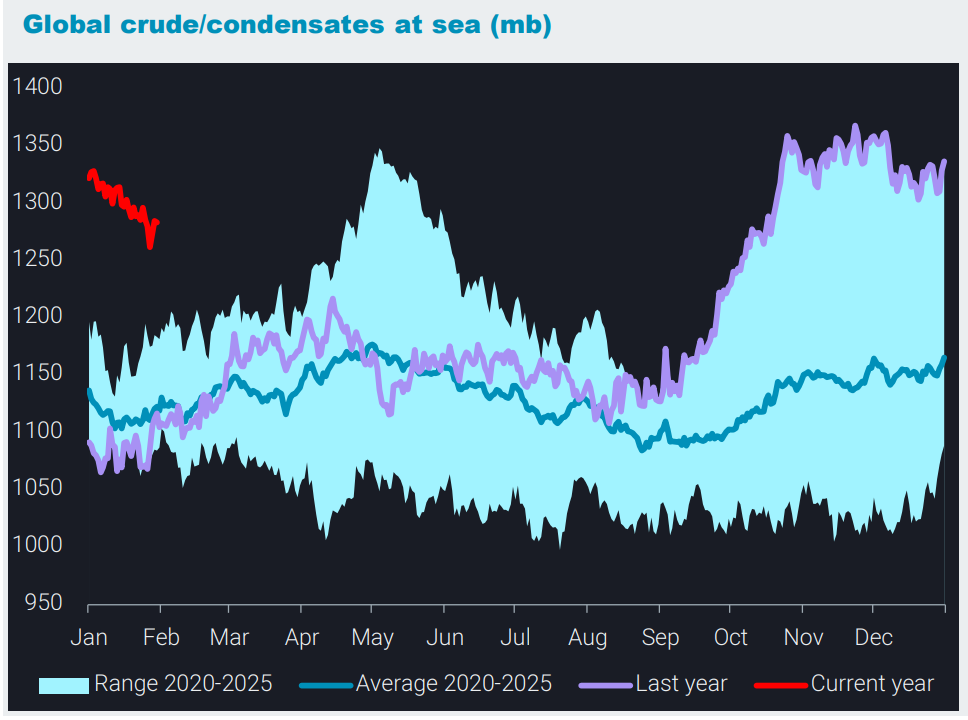

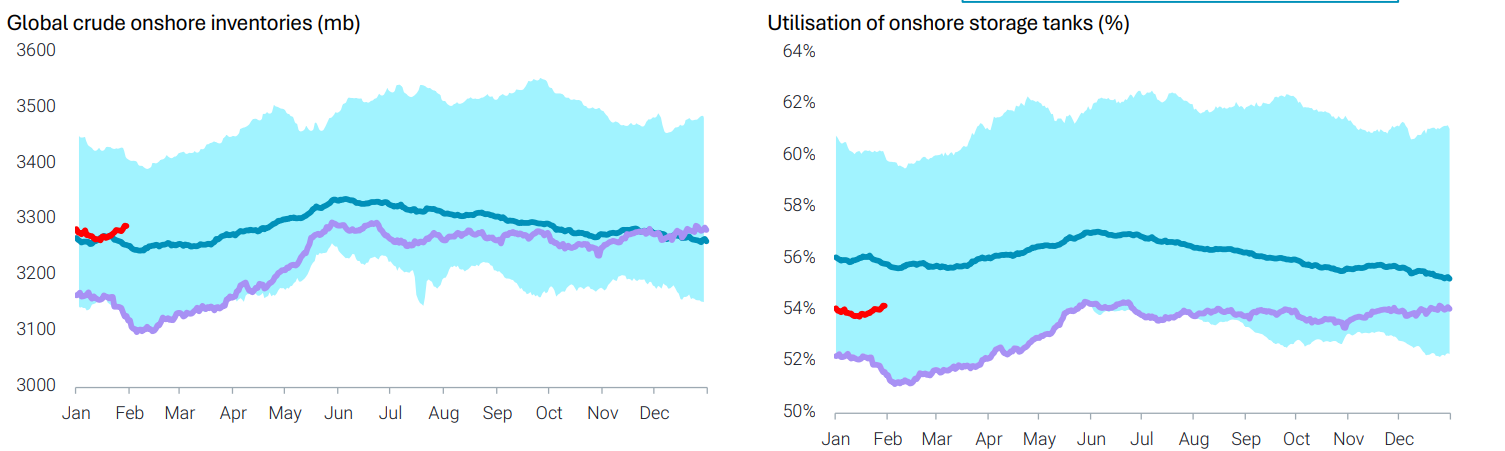

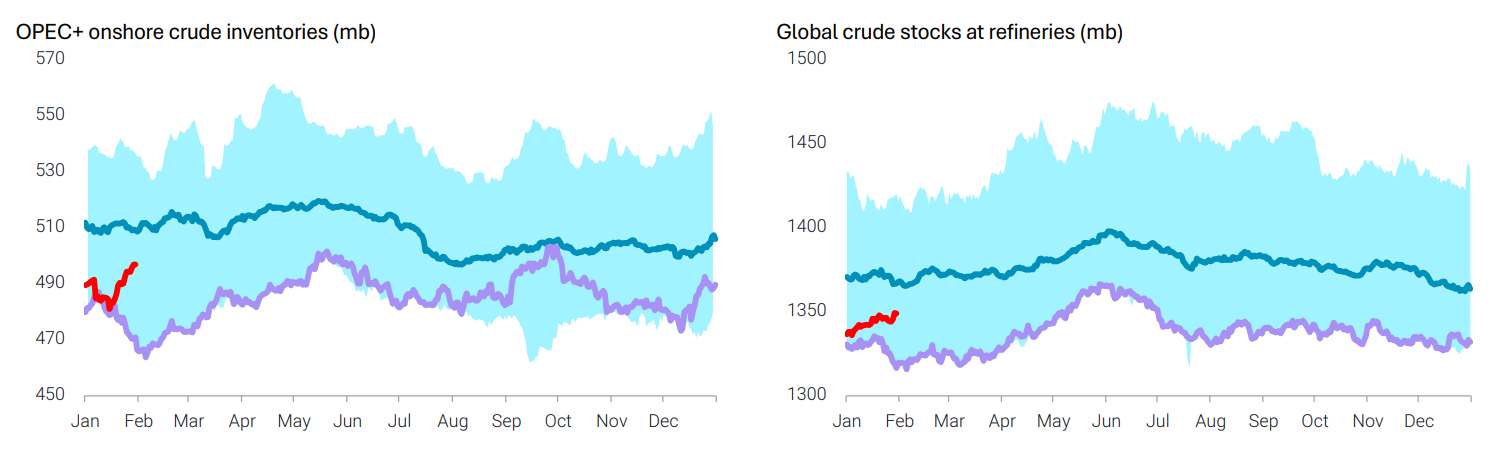

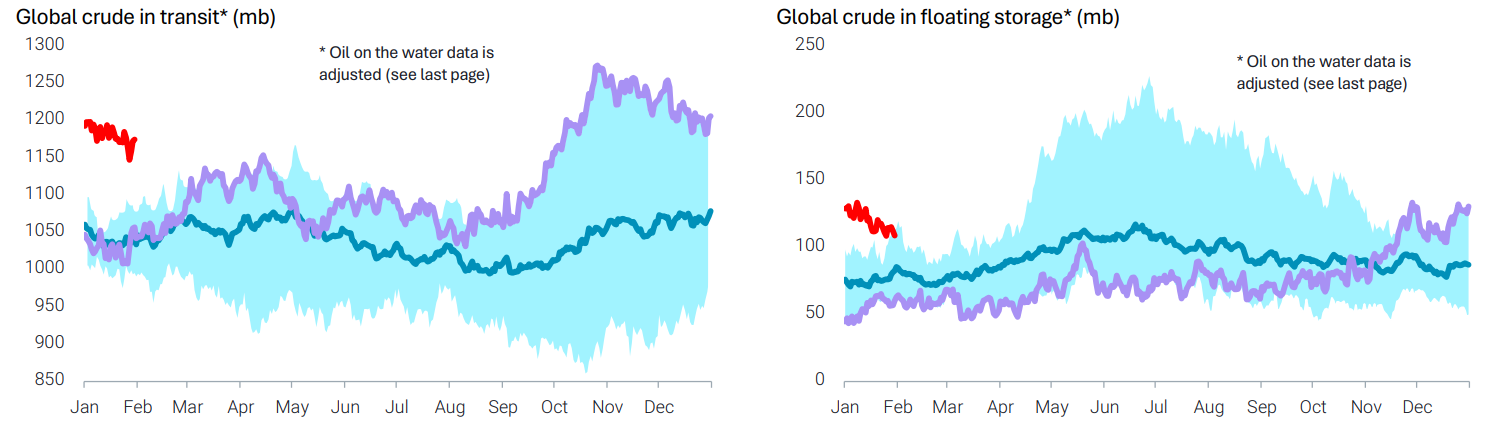

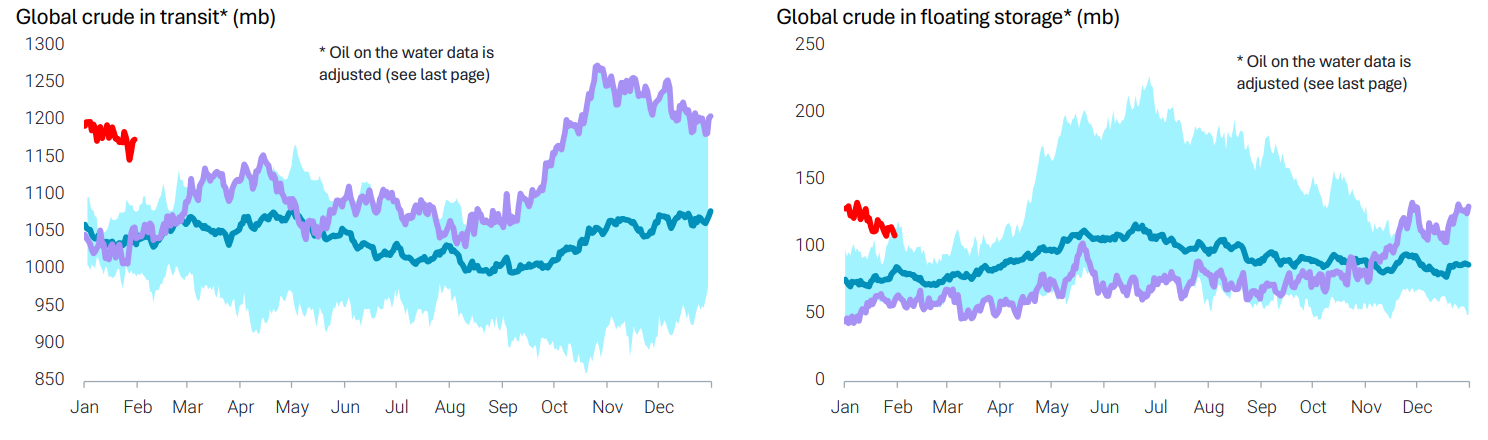

As we looked at in the last report ‘Vortex’- what moves from offshore-has to move onshore. Just in time for driving season load-ins for refiners. This now creates a bearish force and sets up all eyes on how aggressive are the refinery runs, gasoline builds/draws etc from the weekly EIA oil reports going forward. Make storage figures relative again. If/When the Iranian risk premium fades, front prices would be 100% exposed to dramatic downside. If you then match this with large US storage builds, we would have to retreat on price. Step forward to the June OPEC meeting, where they may get back to raising production, and you have a market that will find it hard to maintain a strong bid.

Net-Net- EIA Wednesdays are interesting again through Feb/March and watch out for de-escalation in Iran.

OPEC Meeting Sunday

OPEC will hold a meeting this Sunday 1st Feb. It is pricing in that they will maintain production in place ie. no more hikes-through to end of Q1. A surprise/not priced in information- would be that they go back to the price war hikes started last year in April -read ‘The Real Game’. It was quite puzzling at the time (April 2025), why OPEC would hike production into a weak tariff battered market, despite their plans to maybe bring back production. The market was weak, however it could be read no other way than the start of a market share war.

I then followed up in October last year in The OPEC Game-where there were signs that OPEC could not actually get production back to the headline hike levels. While these headlines were a shock to front pricing,, the actual throughput of production increase was a mere 700kbpd- apparent by November. So they allowed members to voluntary cut by total 1.65mbpd.

Will there be a surprise at this Sunday’s meeting? I rate it below 5% probability. If they want to press their advantage, they will want to re-raise supply/the glut, just as it is starting to drain. The actual ability to do so is highly doubted. The member countries are still probably struggling to max out production.

OPEC required production in February and March this year

10.103 million barrels per day for Saudi Arabia,

9.574 million barrels per day for Russia

4.273 million barrels per day for Iraq

3.411 million barrels per day for the UAE

2.580 million barrels per day for Kuwait

1.569 million barrels per day for Kazakhstan

971,000 barrels per day for Algeria

811,000 barrels per day for Oman

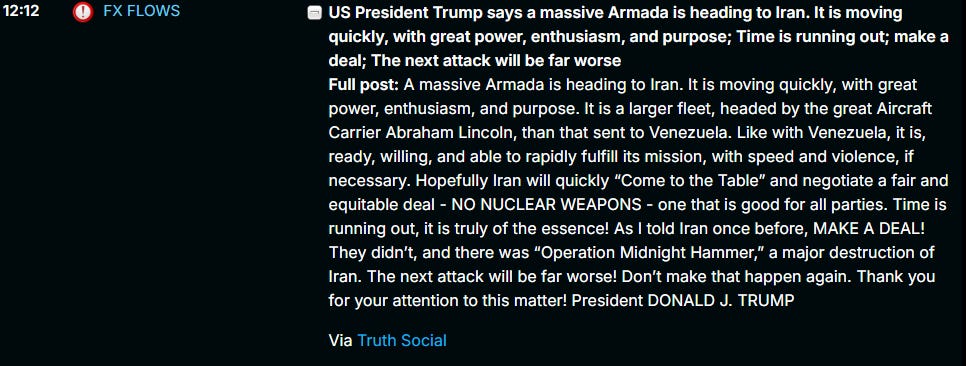

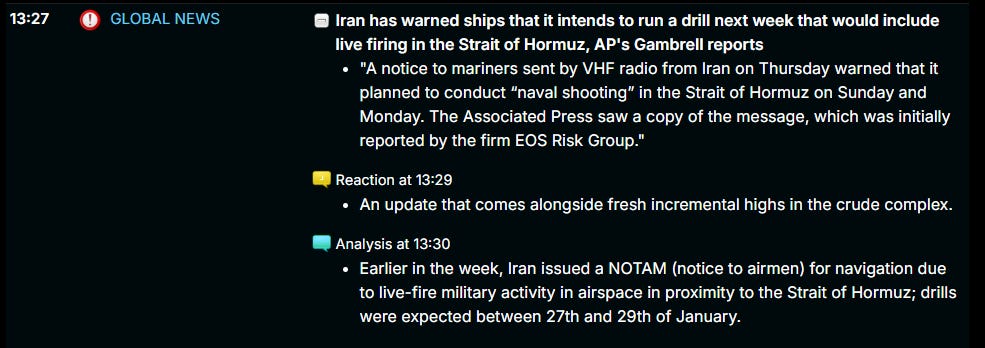

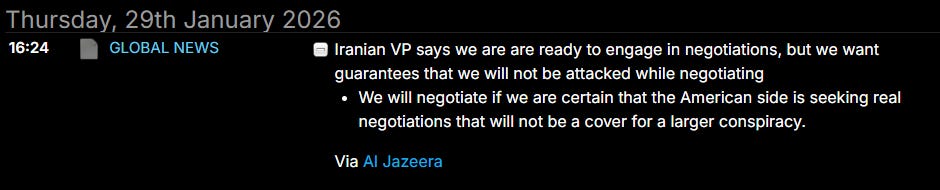

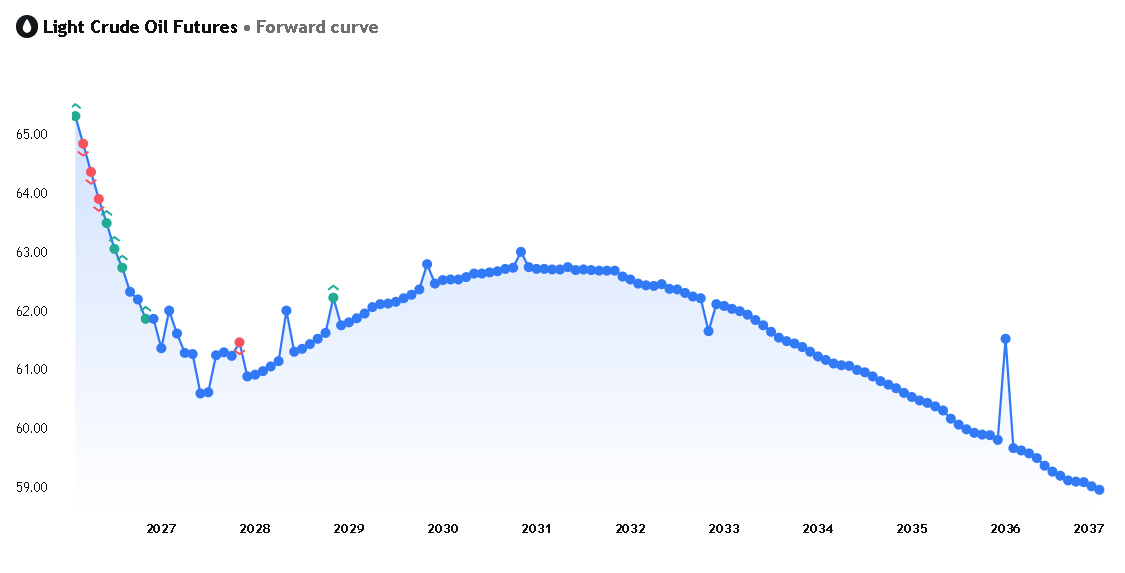

The Iranian situation, while heating up, still lingers with no engagement. This weekend may change that. It has been enough to push the entire curve back into backwardation.

Inflation

Keep reading below for COT data analysis and trade sections.

On Friday-amongst the mix of Warsh getting the Fed chair role- CPI came out hot! So guess hat happens when you have oil up 7% in a week-set to move higher again? You have energy cost led inflation. It’s going to be fun seeing how the markets deal with what most probably will be another PPI/ CPI beat next month . PCE Feb 20th is going to be great craic!

Commitment Of Traders Report

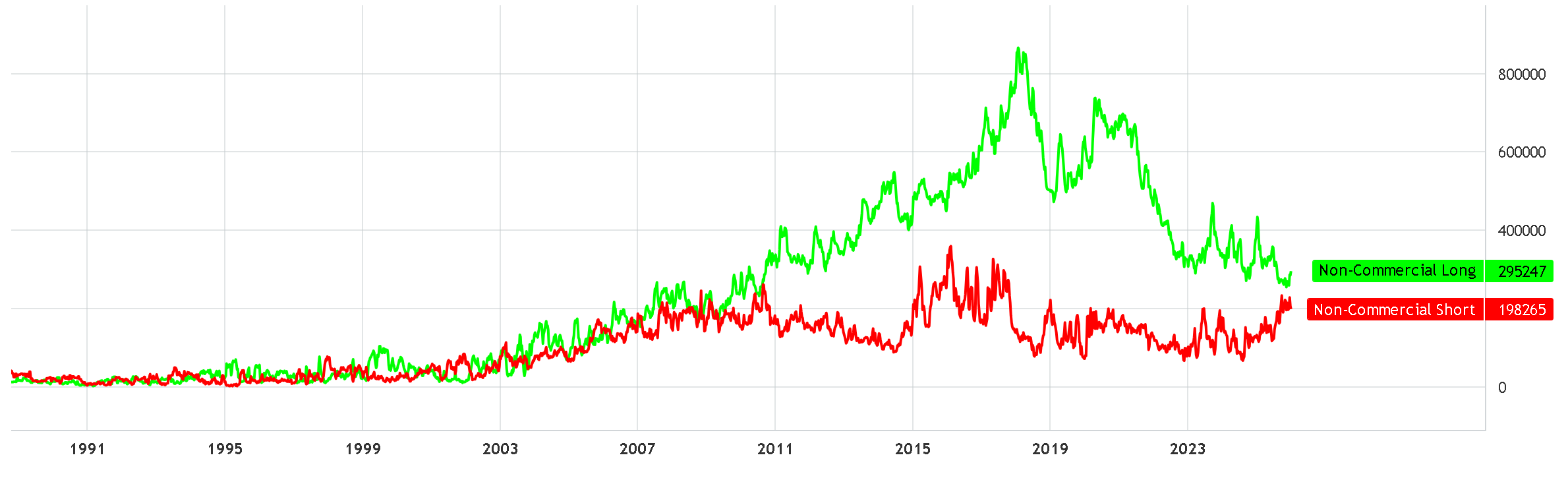

On the whole, there is not much to see. Most of the very signicant COT movements have been in the last 3 reports. We are simply extending what happened 3 weeks ago.

Commercials are increasing shorts, as is expected as prices rise. They are hedging. Specs have indeed asked for another sick bag from the flight attendant, flattening out another 10,882 shorts.

Open interest. +146,788| Total 2,585,126

Commercials Long +39,269 | Total 972,470

Commercial Short +56,559 | Total 1,155,334 - Hedging into higher price

Non Comm Long +5,237 | Total 298,732

Non Comm Short -10,882 | Total 137,078 -more puking

Commercials

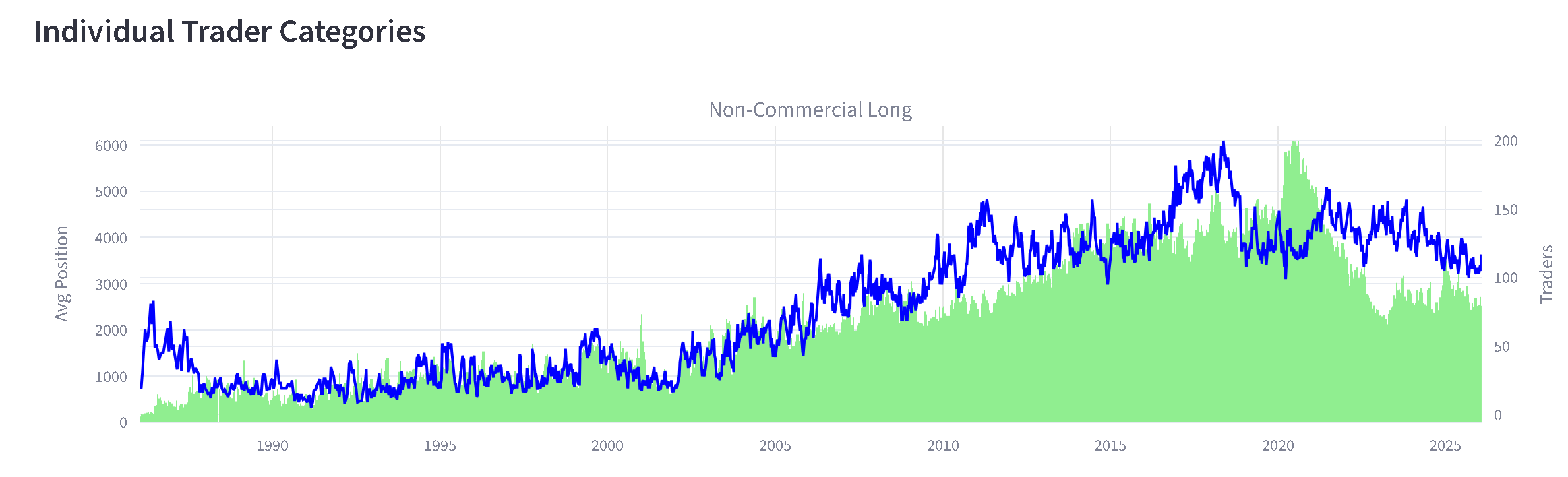

Non-commercials/ Specs/ Managed Money

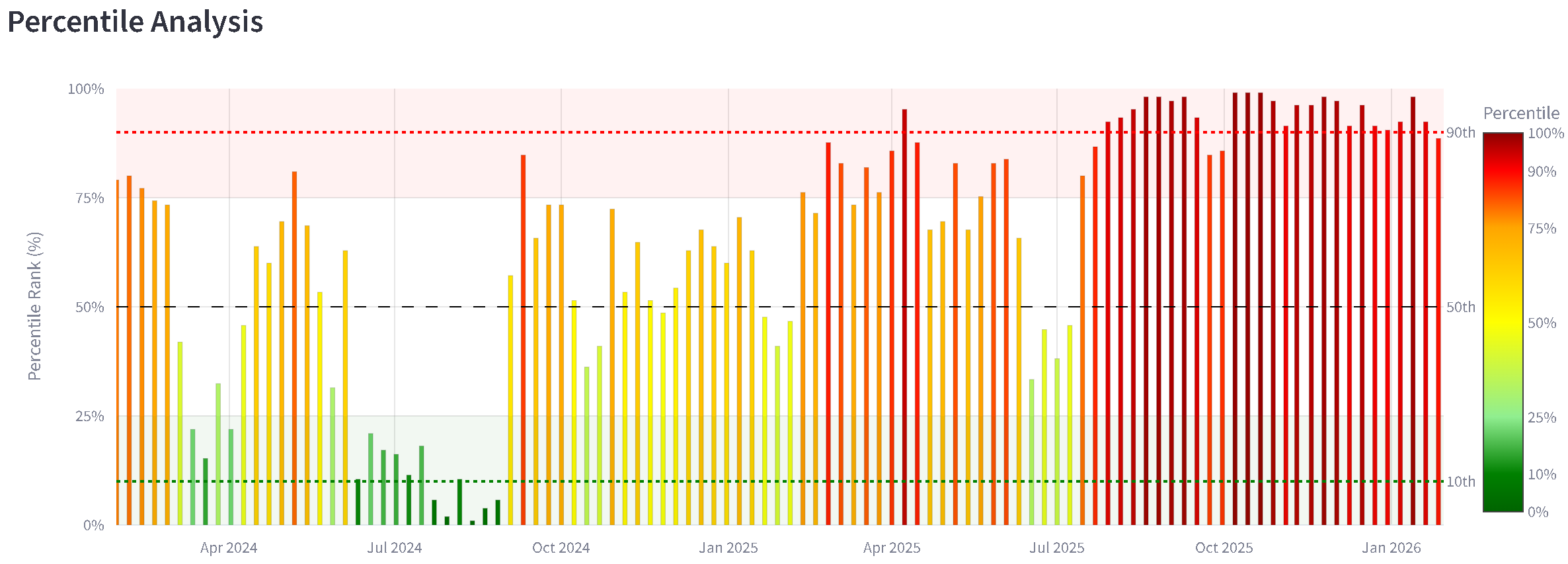

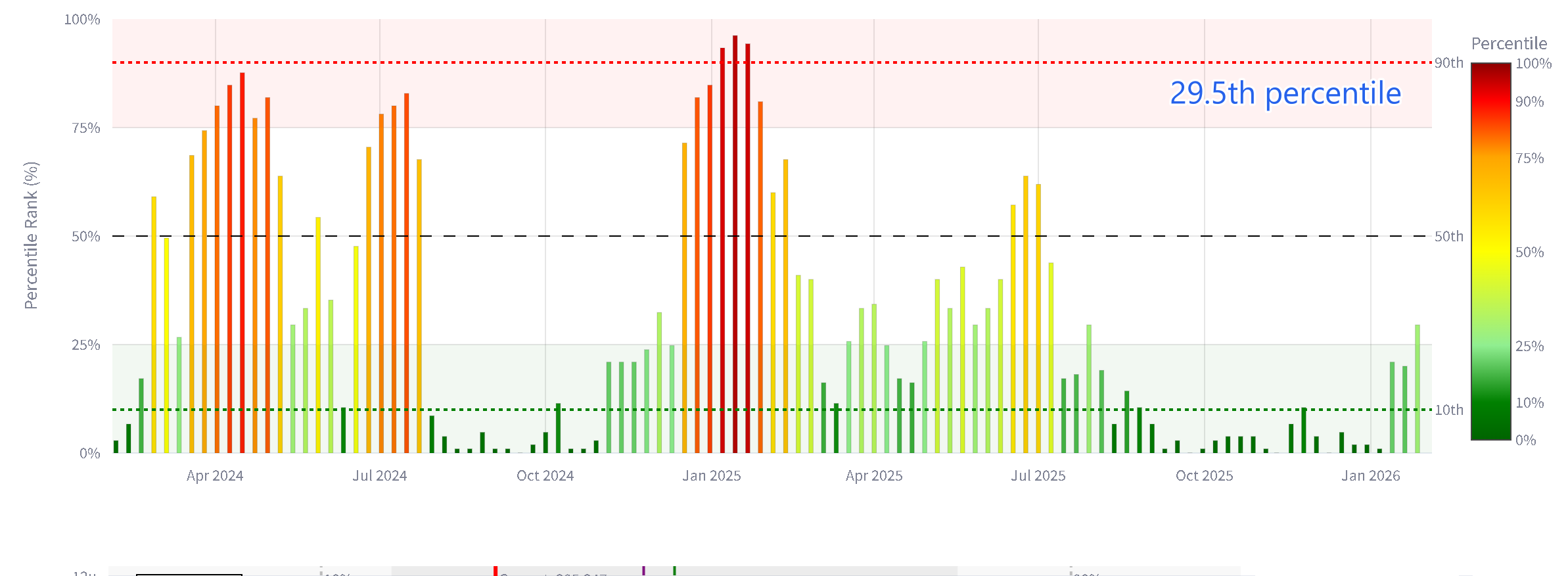

Spec shorts have retreated further as expected from 98.1% 3 weeks ago to 88.9th percentile.

HFI research has been commenting that specs are very long, that may be the case on Brent, but not on WTI NYMEX. With Managed money only at 25th% in longs.

TRADE

The main price driver for the electronic open and next weeks trade is Iranian premium. We have had a phenomenal run this year and it’s only the 1st 30 days. Our seasonal look back tools go back over 30 years. They show there is a seasonal pullback that starts this Monday. We will not be ignoring this. There are many ways then to trade around core positions if we have a strong hypo and good market price content. This report is guidance to you to not sleep on this information.

As mentioned above, Iran and the specs short puke has allowed us to move up quite fast. Should negotiations open up over the weekend between The White House and Iranian officials-this will cause a significant pullback and pricing out of upside premium seen last week. Then if we get to Wednesdays EIA data and see large builds- its going to be a rinse out of weak longs.

So here is what I’m looking for.

A) Iranian de-escalation scenario

B) Iranian no change/escalation scenario

No change is as good as risk premium remaining. I see this as being most probable by electronic and Monday pitt session open.

I like this ‘no change’ trade setup as it would prove the imbalance up area of MPVAH, to then trigger other systems and load up long. Would have to see this on the ladder as confirmation of other sized participants. Best scenario would be to see large sellers attacking the buyers here and get absorbed/fail.

Well. That about does it. I’ll update COT Monday when possible.

Trading is waiting.

Tim